How to Save Tax in India If You Earn ₹1.5–2 Crore as a Salaried Employee

Fewer than 4 lakh people in India file tax returns showing income between ₹1–5 Cr. About half of them are salaried. If you're earning ₹1.5–2 Cr from a job, you're in a group so small that most tax advice online simply isn't written for you — and the system offers you remarkably little compared to business owners in the same bracket.

You're paying one of the highest effective tax rates in the country. The standard advice — 80C, ELSS, PPF — is either unavailable under the new regime or too small to move the needle at this income level.

This article covers every verified, legal option available to a salaried person at this income level, what each one actually saves, and what to ignore.

First: Understand Your Actual Tax Rate

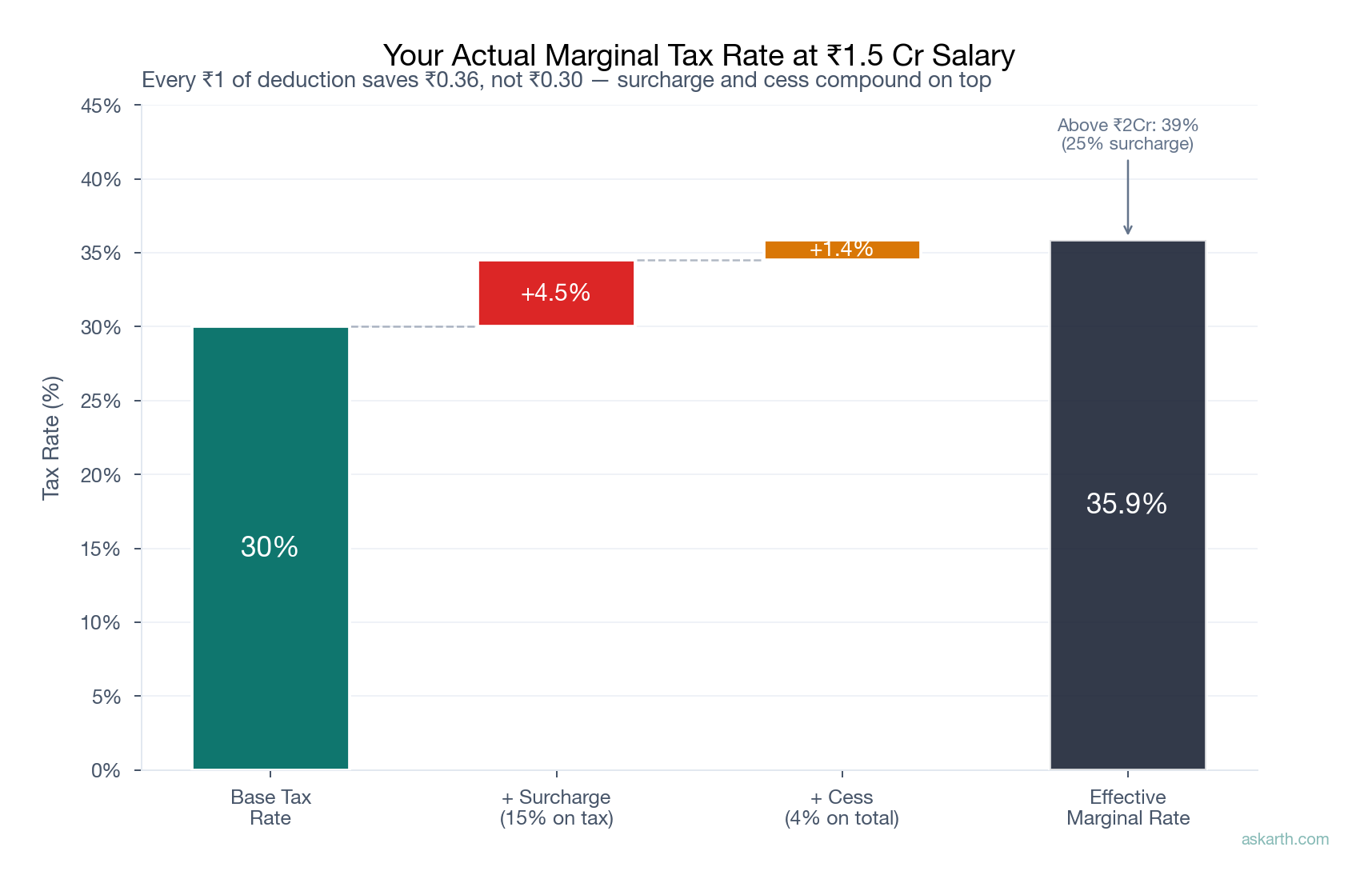

At ₹1.5–2 Cr of salary income, your effective tax rate isn't 30%. It's higher — because of surcharge.

India applies a surcharge on top of the base tax rate:

| Income | Surcharge |

|---|---|

| Above ₹50L | 10% |

| Above ₹1 Cr | 15% |

| Above ₹2 Cr | 25% |

Add 4% health and education cess on top.

At ₹1.5 Cr, your effective rate is approximately 38–39%. This matters because every rupee of deduction you legitimately claim saves ₹0.39, not ₹0.30. The math on every option below changes accordingly.

What Actually Works

1. Employer NPS Contribution — Section 80CCD(2)

This is the single most powerful tax lever available to salaried employees under the new regime — and the most commonly missed.

Your employer can contribute up to 14% of your basic salary to NPS on your behalf. This amount is: - Fully deductible from your taxable income - Available under the new tax regime (unlike most other deductions) - Outside the ₹1.5L Section 80C ceiling

Example: Basic salary of ₹60L/year → 14% = ₹8.4L deduction → at 39% effective rate, that's approximately ₹3.3L saved annually.

The catch: your employer has to offer it, and you typically need to ask HR to activate it. The money is locked in NPS until retirement (with limited partial withdrawal options), so treat this as a retirement savings vehicle, not a liquidity tool.

If your employer offers NPS and you haven't activated it, this is the first thing to fix.

2. Car Lease Through Employer

If your employer has a car lease program, the EMI is deducted from your pre-tax salary. The taxable perquisite value is only a nominal amount — ₹1,800–₹2,400/month depending on engine size, plus ₹900/month if a driver is provided.

Example: On a ₹1L/month car lease, you pay tax on ~₹2,400 instead of ₹1L. At 39%, that's a saving of roughly ₹4.5L/year on a ₹12L/year lease.

This works under both old and new tax regimes. The limitation: not all employers offer structured lease programs. If yours does and you're planning to buy a car anyway, leasing through the employer is almost always better than buying with post-tax money.

3. Flexi Benefits — Claim Everything in Your CTC

Most large employers offer a flexible benefits basket as part of CTC. These components are either fully exempt or taxed at a nominal perquisite value:

| Component | Annual Limit | Tax Treatment |

|---|---|---|

| Meal coupons/vouchers | ₹1,05,600 (₹8,800/month) | Fully exempt |

| Mobile/internet reimbursement | Actual bills | Fully exempt |

| Laptop/gadget reimbursement | Actual cost | Fully exempt (employer-owned) |

| Books and periodicals | Actual cost | Fully exempt |

At ₹1.5 Cr income, every rupee of flexi benefits you don't claim is taxed at 39%. If you have ₹3L in unclaimed flexi components, that's ₹1.17L in unnecessary tax paid every year.

Check your CTC structure. If you're not claiming your full flexi basket, talk to your HR or payroll team before the financial year ends.

4. Home Loan Interest on Let-Out Property — Section 24

If you own a property that's rented out, the full interest on the home loan is deductible with no upper cap under Section 24. This is available even under the new tax regime.

Example: ₹2 Cr home loan at 9% → ~₹18L interest in year 1 → at 39% effective rate, approximately ₹7L in tax savings.

Note: the self-occupied property deduction (₹2L cap) is only available under the old regime and is largely irrelevant at this income level. A let-out property with a large loan is a different story — it's a genuine, uncapped deduction that also builds an asset.

5. ESOP and RSU Timing

If you have equity compensation — common at this income level in tech, finance, and startups — the tax treatment has two stages:

At vesting/exercise: Taxed as salary income (FMV at vest minus exercise price). This gets added to your salary income and affects your surcharge bracket.

At sale: Taxed as capital gains. - Listed shares held >12 months: LTCG at 12.5% - Listed shares held <12 months: STCG at 20%

(Budget 2024 revised these rates, effective July 2024.)

Where planning helps: - Spread vesting or sale across financial years to avoid income bunching in a single year — crossing from the 15% to 25% surcharge bracket costs you significantly - Hold shares for >12 months after vesting to qualify for LTCG rates - Capital losses from other assets can be set off against ESOP/RSU capital gains

This requires coordination between your equity plan schedule and your tax filing. A CA who understands equity compensation is worth the cost.

6. Capital Gains Harvesting

If you hold equity mutual funds or stocks with unrealized long-term gains, you can sell up to ₹1.25L of LTCG per year tax-free (the annual LTCG exemption). Sell and immediately rebuy to reset your cost basis.

At 12.5% LTCG rate, this saves ₹15,625/year. Small, but it costs nothing and takes 10 minutes once a year.

7. Standard Deduction

₹75,000 flat deduction under the new regime for salaried employees. Automatic — no action needed. Just confirm with your employer that you're on the new regime (it's the default, but worth verifying).

What to Ignore

A lot of tax-saving advice circulates online that either doesn't apply at this income level or is simply incorrect. Here's what to skip:

80C investments (₹1.5L limit): Under the new regime, 80C deductions don't apply. Under the old regime, ₹1.5L is a rounding error on a ₹1.5 Cr income. Not worth optimizing around.

NPS own contribution — 80CCD(1B) (₹50K): Only available under the old regime. At ₹1.5 Cr income, the old regime almost never makes sense. This deduction is largely irrelevant for this group.

HUF for salary income: Salary income cannot be transferred to an HUF. HUF is only useful if you have investment income, rental income, or business income that genuinely belongs to the family. It does not reduce salary tax.

Showing salary as business income: Not possible. Your employer files TDS under Section 192 as salary income. You cannot reclassify it as business income to claim 44ADA benefits — this is a common misconception.

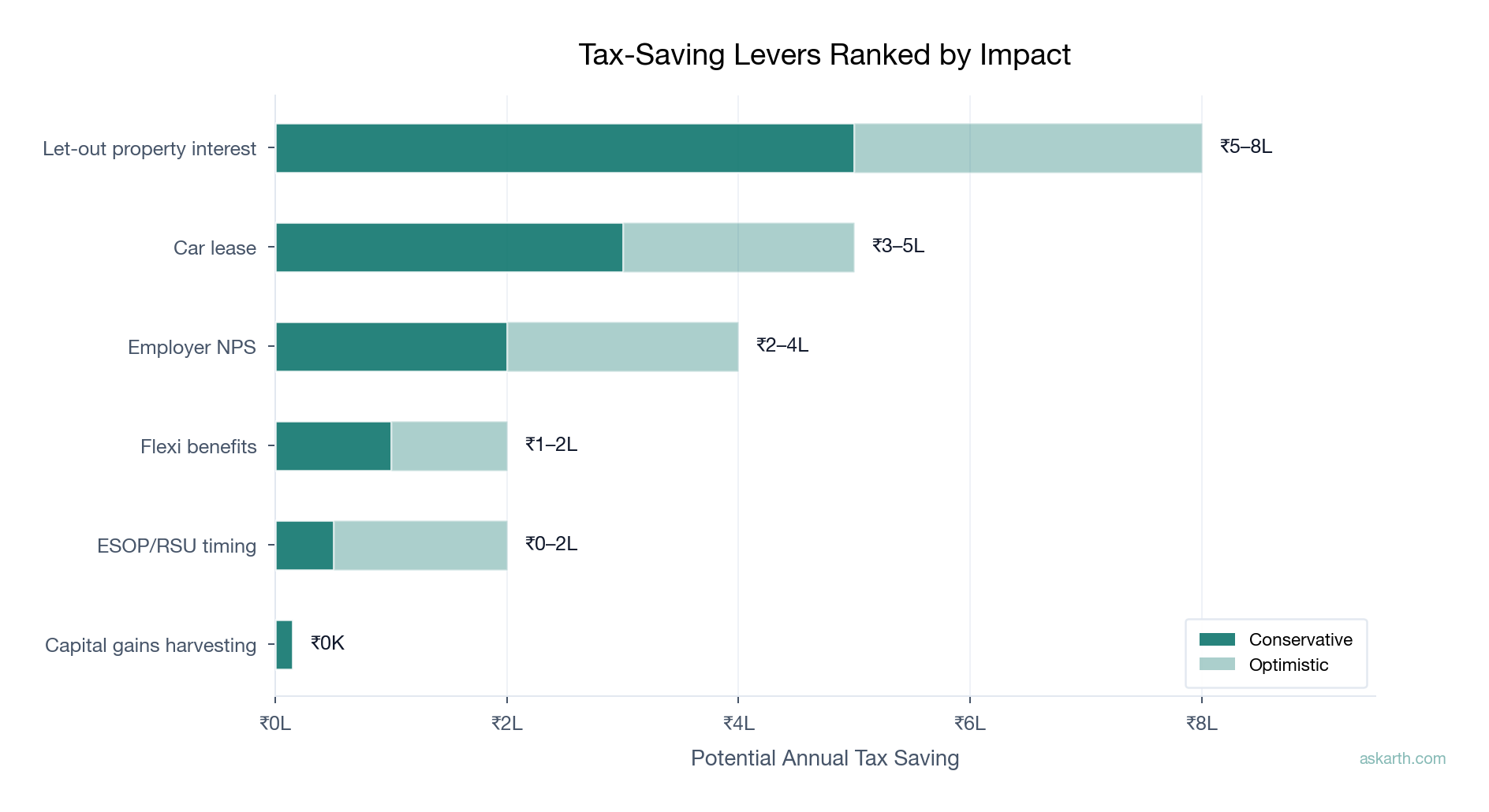

The Realistic Numbers

Here's what a salaried person at ₹1.5 Cr can actually save annually with all legal levers combined:

| Lever | Potential Annual Saving | Conditions |

|---|---|---|

| Employer NPS (14% of basic) | ₹2–4L | Employer must offer it |

| Car lease | ₹3–5L | Employer must have a lease program |

| Flexi benefits (unclaimed) | ₹1–2L | Depends on what's unclaimed in your CTC |

| Let-out property interest | ₹5–8L | Must own a rented property with a home loan |

| ESOP/RSU timing | Situational | Depends on equity comp structure |

| Capital gains harvesting | ~₹15K | Small but free |

Realistic total: ₹6–15L/year, depending on your employer's flexibility and whether you own property.

On a tax bill of ₹50–60L, that's a 10–25% reduction. Meaningful — but not the dramatic savings that business owners or freelancers can achieve through expense deductions and entity structuring.

The Bottom Line

For a pure salaried person at ₹1.5–2 Cr, the options are genuinely limited. The system offers very little compared to what's available to business owners. The levers that do exist — employer NPS, car lease, flexi benefits — require your employer to offer them, and ideally need to be negotiated into your CTC structure before you join.

The practical checklist:

- Activate employer NPS if your company offers it — this is the highest-impact move

- Use the car lease program if you need a car and your employer has one

- Claim every flexi benefit in your CTC — don't leave it as taxable cash

- Time your ESOP/RSU sales across financial years if you have equity compensation

- Work with a CA who understands high-income salaried taxation, not a generic filing service

Beyond these, the honest answer is: you're going to pay a large tax bill. The better use of energy is making sure your post-tax investments are structured efficiently — and that you're not leaving the legitimate savings above on the table.

Sources: Income Tax Act 1961 (Sections 80CCD, 24, 115BAC), CBDT notifications, ClearTax (cleartax.in), Income Tax India portal (incometax.gov.in) Last verified: May 2026 Disclaimer: Tax rules and surcharge rates change with each Union Budget. Verify current slabs and limits on incometax.gov.in. This is not personalized financial advice — consult a CA for your specific situation.

Run these numbers on your finances

Arth looks at your full picture and tells you what actually matters.

Try Arth →