Switching from a regular mutual fund plan to a direct plan saves you 0.5–1.25% in annual expenses — money that compounds into lakhs over a decade. The process is straightforward, but it triggers a tax event you need to plan for. Here's the tax math, smart strategies, and when it actually makes sense.

Why Switch? The Cost Difference in Real Numbers

Every mutual fund scheme in India has two versions — regular and direct. Same portfolio, same fund manager, same returns before expenses. The only difference: regular plans pay a commission to your distributor (0.5–1.5% annually), which is deducted from your returns via a higher expense ratio.

Not sure whether direct or regular is right for you? Read our full comparison first. Already decided? Keep reading for the how-to.

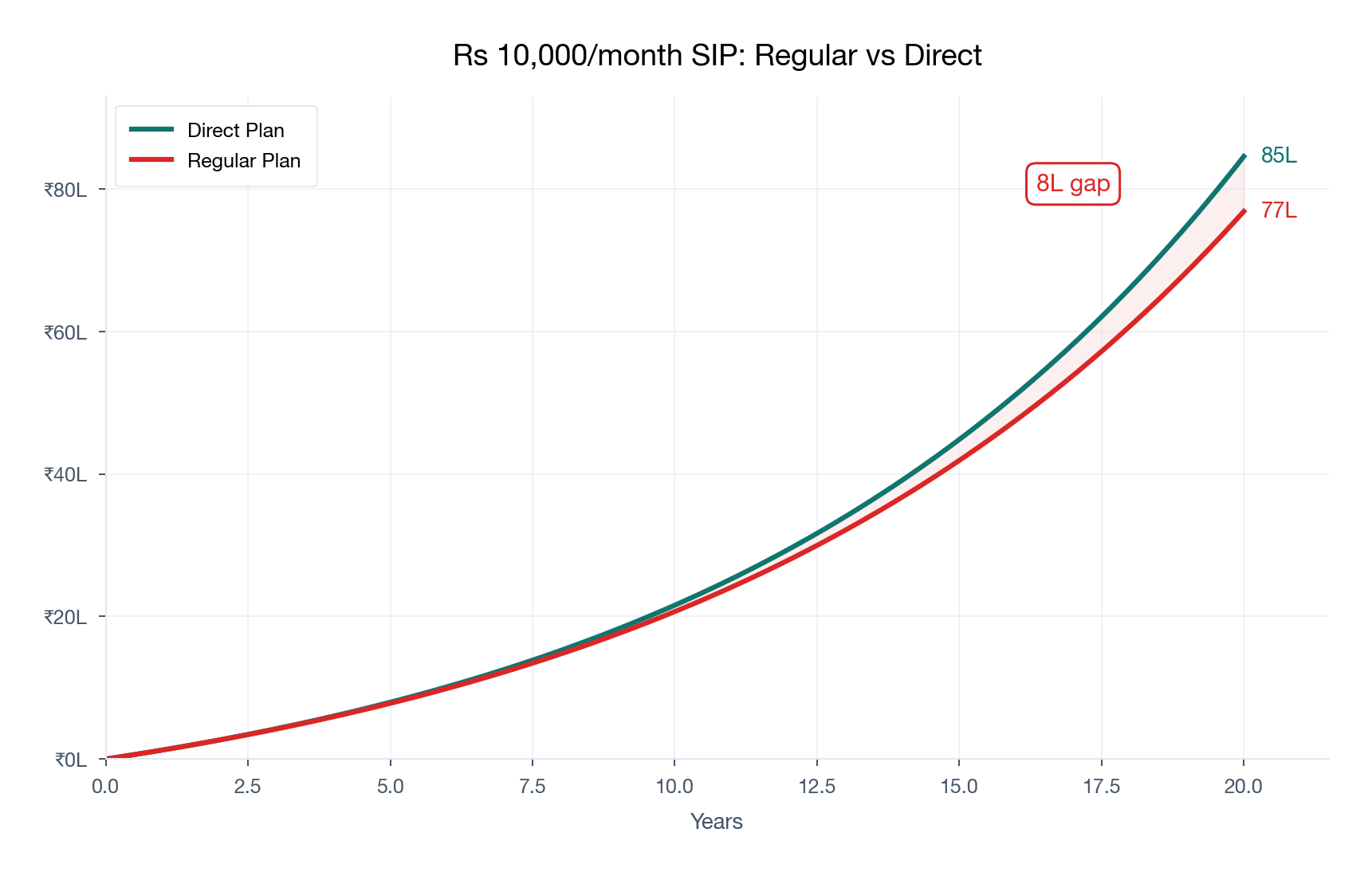

On a ₹10,000/month SIP over 10 years in a typical flexi-cap fund: - Regular plan corpus: ~₹23.2 lakh - Direct plan corpus: ~₹24.4 lakh - Gap: ~₹1.2 lakh (and it widens every year)

Over 20 years, this gap grows to ₹7-8 lakh on a ₹10K SIP — and much more on larger amounts. The expense ratio difference looks small (0.5–1.25%), but compounding turns it into serious money. We ran the exact ₹ math on 5 popular funds using real NAV data — the results are worse than you'd expect.

The Tax Reality: Switching Is a Redemption

Here's what most people don't realize: there's no "free switch" button. SEBI treats a switch from regular to direct as a redemption (sell) of your regular plan units followed by a fresh purchase in the direct plan. This means capital gains tax applies.

Current Tax Rules (FY 2026-27)

| Fund Type | Holding Period for LTCG | LTCG Tax | STCG Tax | Exemption |

|---|---|---|---|---|

| Equity funds (>65% equity) | >12 months | 12.5% | 20% | ₹1.25 lakh/year |

| Debt funds (bought after Apr 2023) | Any | Slab rate | Slab rate | None |

| Hybrid funds (>65% equity) | >12 months | 12.5% | 20% | ₹1.25 lakh/year |

| Hybrid funds (<65% equity) | >24 months | 12.5% | Slab rate | None |

Key point: For equity funds, gains up to ₹1.25 lakh per financial year are tax-free. If your total gains across all equity switches are below this threshold, you pay zero tax.

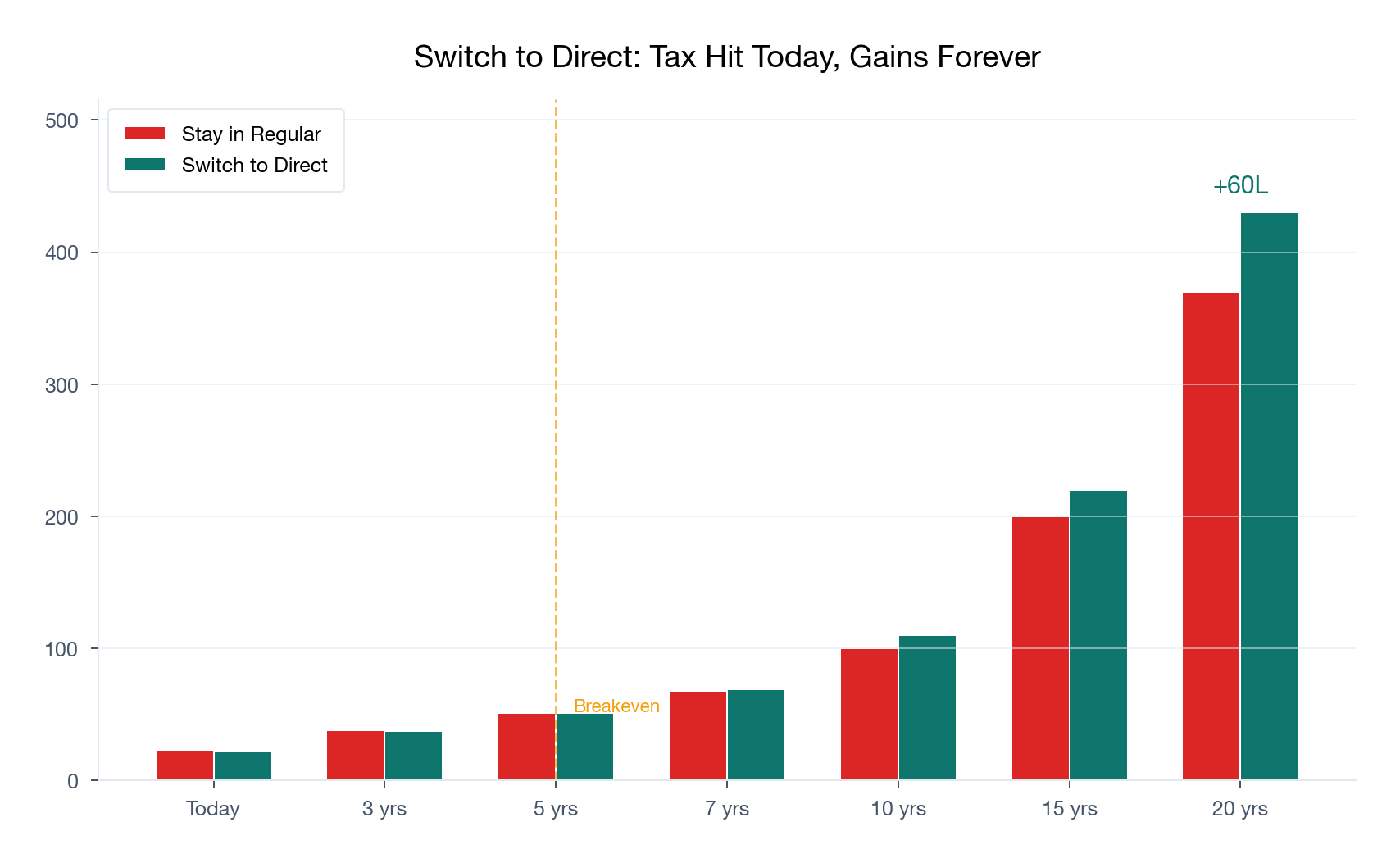

The Breakeven Math: How Long to Recover the Tax Hit

Switching costs you tax today but saves you expenses every year going forward. The breakeven depends on whether you owe tax at all.

If your total LTCG is under ₹1.25 lakh: Breakeven is Day 1. You pay zero tax and start saving immediately.

If you owe tax: The breakeven is roughly 4-5 years regardless of corpus size — because both the tax hit and the annual saving scale proportionally with your portfolio. After that, direct pulls ahead and the gap only widens.

Rule of thumb: If your remaining investment horizon is 5+ years, switching almost always makes sense for equity funds. The tax is a one-time cost; the expense saving recurs every year and compounds.

How to Switch (The Mechanics)

The process is the same everywhere — it's a "switch" transaction (redeem regular, buy direct, same fund):

- Via AMC website: Log in → Transactions → Switch → Select regular plan as source, direct plan as target

- Via platforms (Kuvera, Groww, INDmoney): Import your external holdings → use their "switch to direct" feature

- Via MF Utilities (mfuonline.com): Works across all AMCs from one place

- Manual: Redeem regular → wait for proceeds (T+2) → reinvest in direct

After switching, cancel your old regular plan SIP separately — the switch doesn't auto-cancel it. Start a new SIP in the direct plan.

Tax-Smart Switching Strategies

Strategy 1: Use Your ₹1.25 Lakh LTCG Exemption

If your total long-term gains are under ₹1.25 lakh, switch tax-free. For larger portfolios, switch in tranches across financial years:

- March-April straddle: Switch ₹1.25L gains worth in March, another ₹1.25L in April (two financial years, ₹2.5L exempt)

- Annual tranches: Switch a portion each year to stay within the exemption

Strategy 2: Switch Loss-Making Units First

Units bought at market highs that are currently at a loss? Switch those first — no tax, and you can even book the loss to offset other gains.

Strategy 3: New SIPs in Direct Immediately

Even if you don't switch existing holdings, start all new SIPs in direct plans today. Zero tax, immediate benefit. Switch the old holdings gradually.

What Happens to Your Distributor?

When you switch to direct, your distributor stops earning trail commission on those assets. You don't need their permission, and they can't block it. Some may call when they see assets moving — you're not obligated to explain or stay.

When NOT to Switch

Switching isn't always the right move:

| Situation | Why You Might Stay in Regular |

|---|---|

| Short horizon (<3 years) | Tax cost won't be recovered in time |

| Getting genuine advisory value | If your advisor does goal planning, rebalancing, crash-time handholding — that's worth the fee |

| Very small corpus (<₹1-2 lakh) | The absolute ₹ saving is negligible; not worth the effort |

| International funds with closed inflows | Some funds have paused fresh purchases due to RBI limits — you can't buy new units in direct |

| Debt funds in 30% slab, short horizon | Tax hit is too high relative to the expense saving |

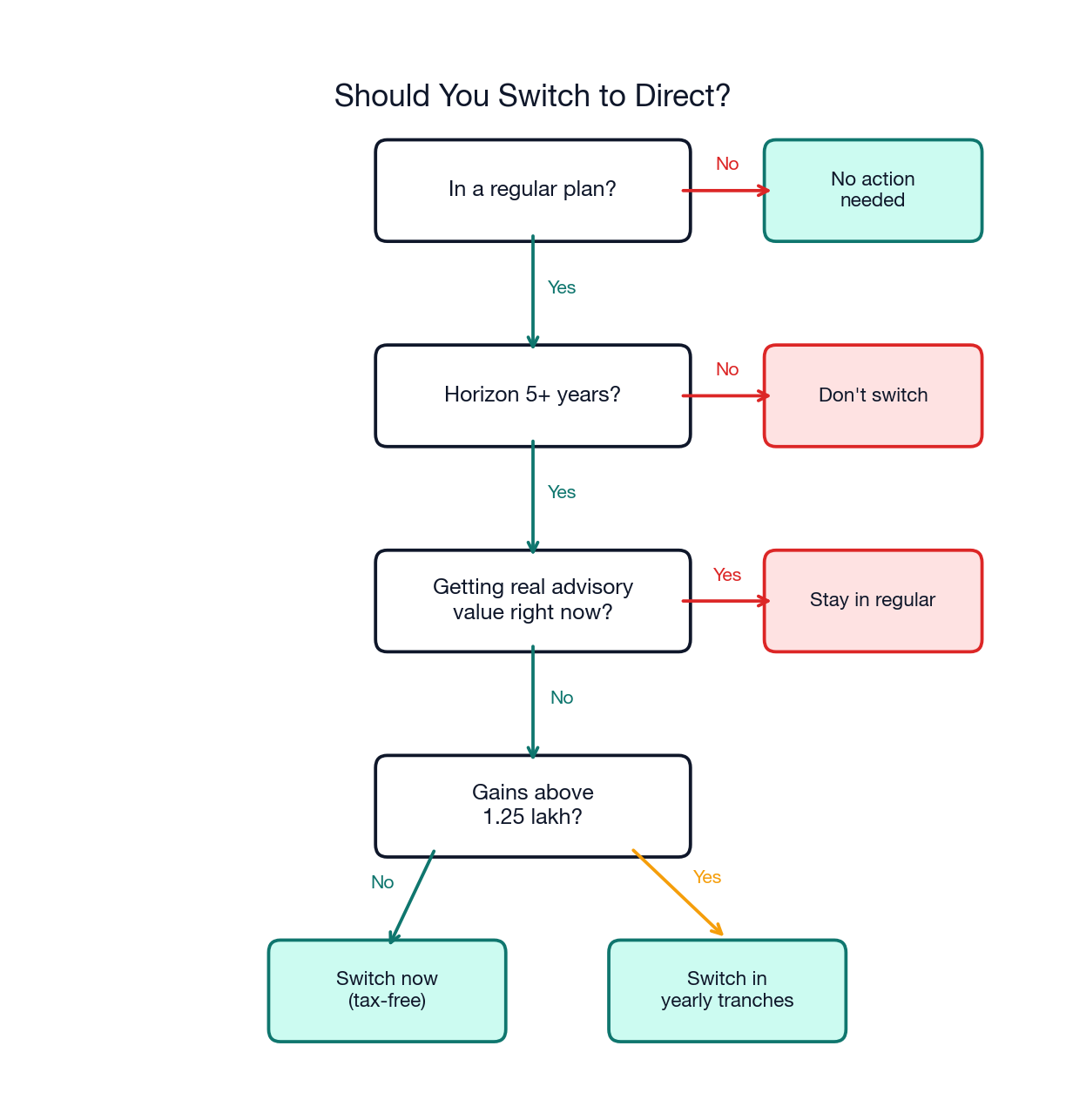

Ask yourself two questions:

- Am I getting real value from my distributor? (Not "did they help me start" — are they helping me now? Regular reviews, rebalancing, crash-time calls?)

- Is my remaining horizon 5+ years?

If the answer is "No" and "Yes" — switch. The math is unambiguous.

Frequently Asked Questions

Can I switch from regular to direct without selling? No. SEBI treats every switch as a redemption + fresh purchase. There's no way to avoid the taxable event. But if your gains are under ₹1.25 lakh, the tax is zero anyway.

How long does the switch take? A switch transaction processes same-day at that day's NAV. If you redeem manually and reinvest, you're out of the market for 1-2 business days.

Will I lose my investment if I switch? No. Your money stays in the same fund, same portfolio. Only the plan variant changes. The only "loss" is the one-time tax on gains (if applicable).

What about the AMFI 12-month cooling-off rule? That applies only when changing from one distributor to another. Switching to direct is not affected — it's immediate.

Should I switch my debt funds too? Be careful. Debt funds bought after April 2023 are taxed at your income slab rate regardless of holding period. Only switch if your horizon is 7+ years or your income is temporarily low.

What to Do Right Now

- Check your holdings: Log into CAMS/KFintech or download your CAS from MFCentral to see which funds are in regular plans

- Calculate your gains: Check if total LTCG is under ₹1.25 lakh (tax-free switch possible)

- Start new SIPs in direct today: Even before switching old holdings, redirect all future investments

- Switch in tranches: Use the ₹1.25L annual exemption across financial years for larger portfolios

- Track the difference: Use a tool like Arth to see your regular vs direct gap in real-time and plan your switch

Sources: SEBI investor education portal, AMFI, Income Tax Act Section 112A (FY 2026-27), Value Research Online Tax rates verified for FY 2026-27 (Assessment Year 2027-28) Note: Tax rules change with each budget. Verify current rates before acting. This is educational content, not tax advice.

Run these numbers on your finances

Arth looks at your full picture and tells you what actually matters.

Try Arth →