Direct plans cost less. Regular plans come with a distributor who may (or may not) add value. The right choice depends on your financial literacy, portfolio size, and whether you actually use the advisory you're paying for. Here's the full comparison with 2026 data.

Direct vs Regular Mutual Fund: The Core Difference

Both plans invest in the exact same portfolio, managed by the same fund manager. The only difference is the expense ratio — regular plans include a distributor commission (0.5–1.5% annually), direct plans don't.

| Direct Plan | Regular Plan | |

|---|---|---|

| Bought from | AMC directly, or via platforms (Groww, Kuvera, Zerodha) | Distributor, bank RM, or agent |

| Expense ratio | Lower (0.5–1.0% for equity) | Higher (1.2–2.0% for equity) |

| NAV | Higher (less cost deducted) | Lower |

| Returns | Higher by 0.5–1.25% annually | Lower |

| Advisory included | No | Depends on distributor |

| Commission to intermediary | None | 0.5–1.5% trail commission |

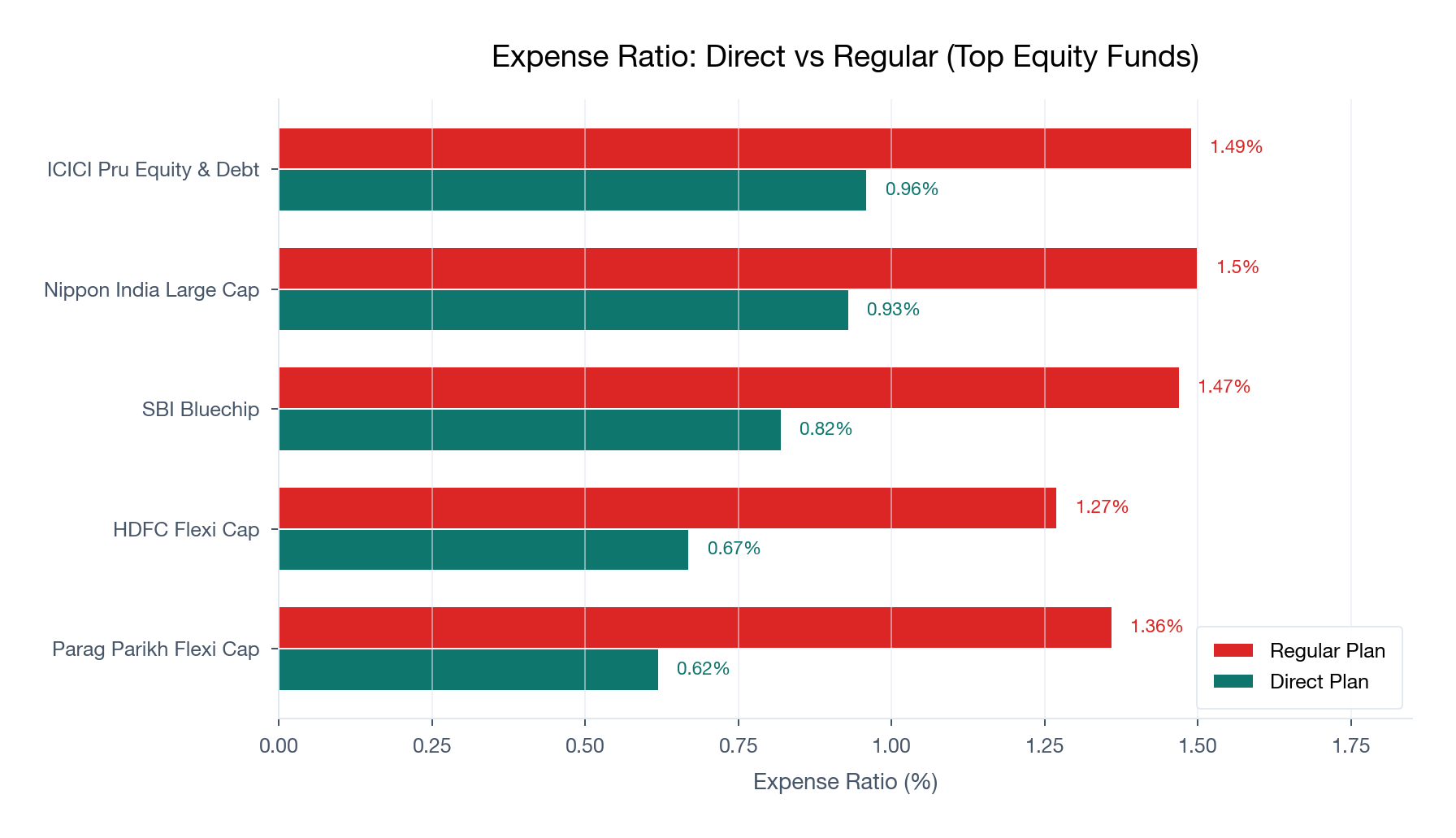

Real Expense Ratios: Top 5 Equity Funds (2026)

| Fund | Direct TER | Regular TER | Difference |

|---|---|---|---|

| Parag Parikh Flexi Cap Fund | 0.62% | 1.36% | 0.74% |

| HDFC Flexi Cap Fund | 0.67% | 1.27% | 0.60% |

| SBI Bluechip Fund | 0.82% | 1.47% | 0.65% |

| Nippon India Large Cap Fund | 0.93% | 1.50% | 0.57% |

| ICICI Pru Equity & Debt Fund | 0.96% | 1.49% | 0.53% |

TER as on April 30, 2026. Source: Fund factsheets via ET Money, Moneycontrol.

The gap ranges from 0.6% to 0.8% for large equity funds. For smaller or thematic funds, it can exceed 1.2%.

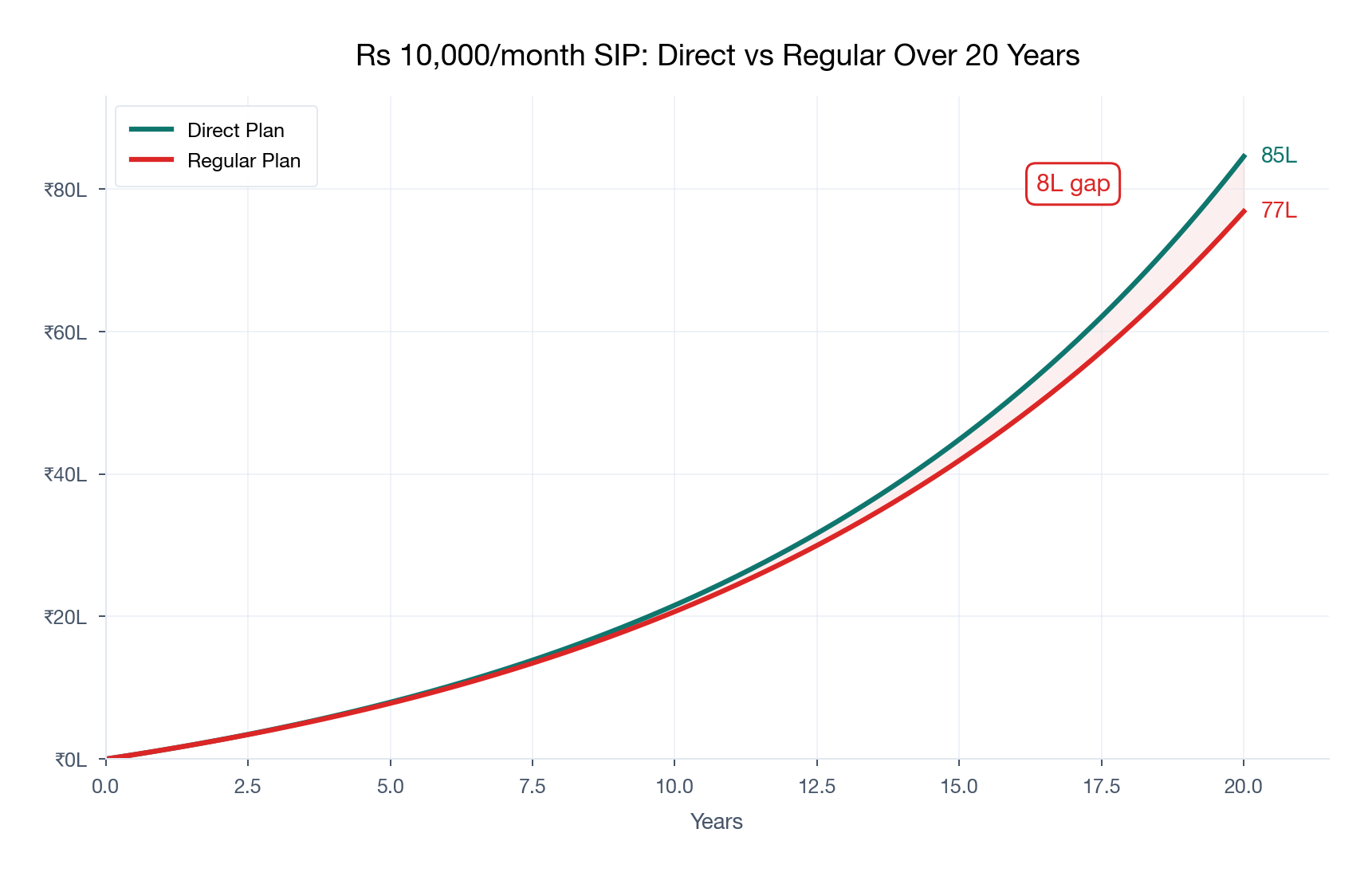

How Much Does This Cost You in Rupees?

A percentage doesn't feel real. Rupees do.

On a ₹10,000/month SIP in a flexi-cap fund (assuming 12% gross return):

| Time Period | Direct Plan Corpus | Regular Plan Corpus | You Lose |

|---|---|---|---|

| 5 years | ₹8.2 lakh | ₹8.0 lakh | ₹20,000 |

| 10 years | ₹24.4 lakh | ₹23.2 lakh | ₹1.2 lakh |

| 15 years | ₹56 lakh | ₹52 lakh | ₹4 lakh |

| 20 years | ₹85 lakh | ₹77 lakh | ₹8 lakh |

On a ₹25,000/month SIP, multiply those gaps by 2.5x. On ₹50,000/month, by 5x.

A 2026 study by 1 Finance Research found that over 10 years, 80% of equity schemes left regular plan investors at least 25% worse off than direct plan investors in the same fund.

We verified this ourselves — our analysis of 5 popular funds using actual NAV data found an average gap of ₹1.58 lakh on a ₹10K SIP.

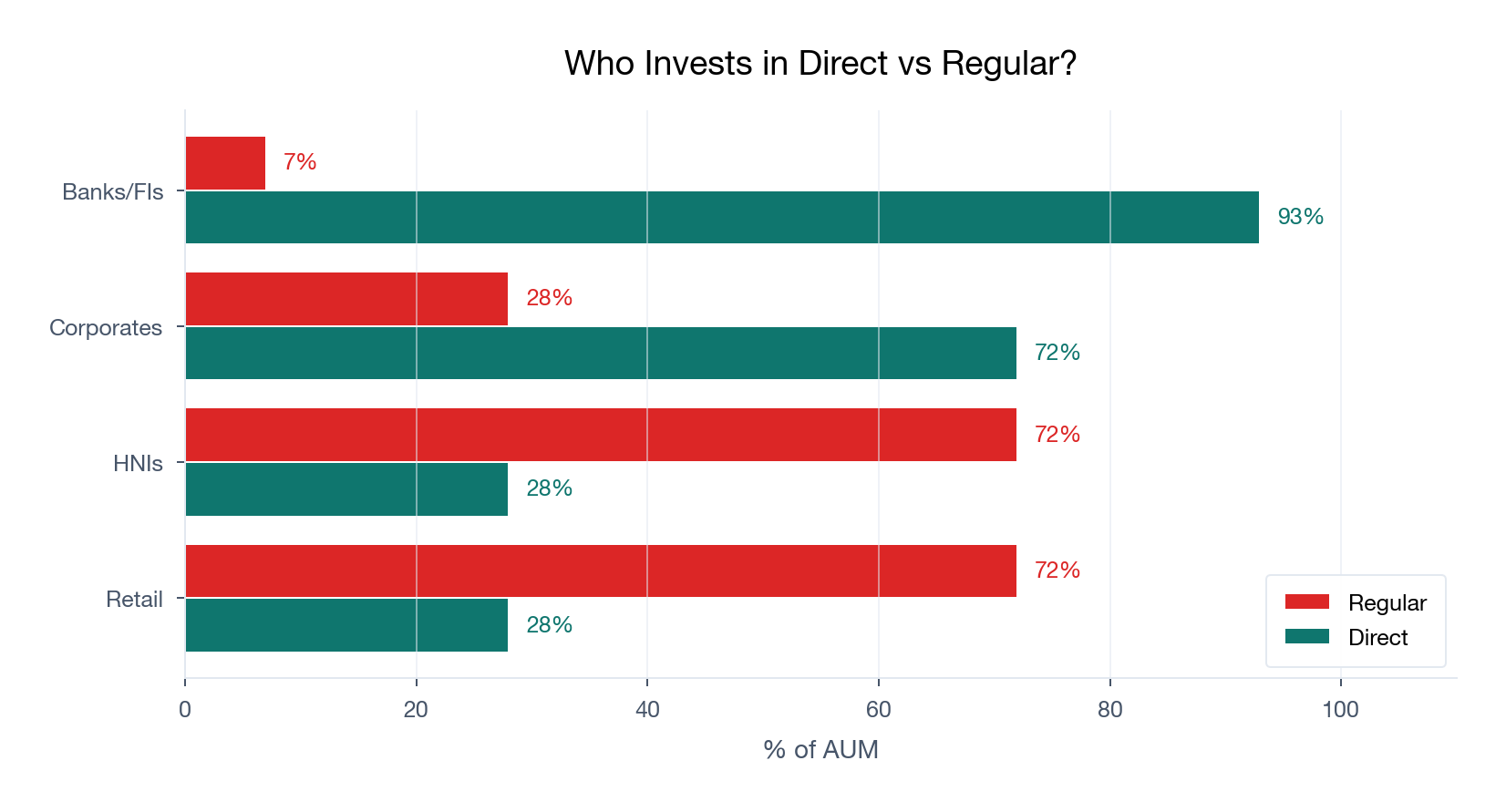

The Industry Split: Who Invests Where?

As of 2025 (AMFI data):

| Investor Type | Direct | Regular |

|---|---|---|

| Retail investors | 28% | 72% |

| HNIs | 28% | 72% |

| Corporates | 72% | 28% |

| Banks/FIs | 93% | 7% |

| Industry total | 48% | 52% |

The 48% direct figure is misleading — it's inflated by corporates parking money in liquid/debt funds. For equity (where retail investors live), 70% still flows through distributors.

When Regular Plans Are Worth It

Regular plans aren't a scam. They bundle advisory into the expense ratio. The question is whether you're actually receiving that advisory.

Regular makes sense when:

- You'd otherwise not invest at all. A distributor who gets you into equity from FDs is worth the 1% — because 11% minus 1% beats 6% in an FD.

- You need behavioral support. Data shows regular plan investors hold longer (21.2% held >5 years vs 7.7% in direct, per AMFI-CRISIL Factbook 2024). If you'd panic-sell without someone calling you during a crash, the fee pays for itself.

- Your portfolio is small (<₹5-10 lakh). A fee-only advisor charges ₹20,000-75,000/year. On a ₹5L portfolio, that's 4-15% — far worse than the 1% regular plan commission.

- You're in a B-30 city with no access to fee-only advisors. The alternative isn't "direct plan" — it's "no investment."

- Your distributor actually does goal planning, rebalancing, and tax optimization. Some do. Most don't.

When Direct Plans Are Better

Direct wins when:

- You're financially literate enough to pick and hold funds. You don't need someone to explain what a flexi-cap is.

- You won't panic-sell in a crash. You've been through at least one 20%+ correction and stayed invested.

- Your portfolio is >₹10-15 lakh. The absolute ₹ savings become meaningful.

- You're using index/passive funds. There's zero alpha a distributor can add to a Nifty 50 index fund.

- Your distributor isn't doing anything. If the relationship is an annual statement and a Diwali greeting, you're paying 1% for nothing.

- You have a long horizon (10+ years). The compounding gap becomes massive.

Direct or Regular: How to Decide

| Question | If Yes → | If No → |

|---|---|---|

| Do you understand mutual fund categories and can pick funds yourself? | Direct | Consider regular (for now) |

| Have you stayed invested through a 20%+ market fall? | Direct | Regular may help with discipline |

| Is your portfolio above ₹10 lakh? | Direct saves real money | Gap is small either way |

| Is your distributor actively advising you (not just selling)? | Regular is fair | You're paying for nothing — switch |

| Are you using index/passive funds? | Direct (no advisory needed) | — |

Direct Plan Platforms in India

If you choose direct, here's where to invest:

| Platform | Type | Key Feature |

|---|---|---|

| AMC websites (SBI MF, HDFC MF, etc.) | Direct from source | No intermediary, but separate login per AMC |

| Kuvera | Aggregator | Free, no commission, all AMCs in one place |

| Groww | Broker + MF | Large user base, also offers stocks |

| Zerodha Coin | Broker + MF | Demat-based MF holding |

| MF Utilities (MFU) | Industry platform | All AMCs, slightly dated UI |

| MFCentral | CAMS + KFintech | Official, download CAS statements |

Already in Regular? Here's What to Do

If you're currently in regular plans and want to move to direct, read our detailed guide: How to Switch from Regular to Direct Mutual Fund (2026 Guide)

Quick version: - Gains under ₹1.25 lakh? Switch tax-free today. - Gains above ₹1.25 lakh? Switch in yearly tranches to use the exemption. - Either way, start all new SIPs in direct immediately — zero tax, instant benefit.

Frequently Asked Questions

Is the NAV different for direct and regular plans? Yes. Direct plan NAV is always higher because less expense is deducted daily. But this doesn't mean direct is "more expensive to buy" — you get fewer units at a higher NAV, and the value is the same. Over time, direct NAV grows faster.

Can I have both direct and regular plans of the same fund? Yes. They're treated as separate folios. Many investors keep old regular holdings while starting new SIPs in direct.

Do direct plans have lower returns? No — the opposite. Direct plans have higher returns because less is deducted as expenses. Same gross return, lower cost = higher net return.

Is there any risk difference between direct and regular? Zero. Same portfolio, same fund manager, same market risk. The only difference is cost.

Who should NOT choose direct plans? Someone who genuinely needs hand-holding — first-time investors who'd otherwise not invest, people who panic during market falls, or those who need comprehensive financial planning bundled in.

Sources: AMFI AUM data, AMFI-CRISIL MF Industry Factbook (March 2024), fund factsheets from respective AMC websites Last verified: May 2026 Note: Expense ratios change periodically. Check current TER on the AMC website before investing.

Run these numbers on your finances

Arth looks at your full picture and tells you what actually matters.

Try Arth →