Your Regular Mutual Fund Cost You ₹1.58 Lakh — Here's the Fund-by-Fund Breakdown

TL;DR: I ran a ₹10,000/month SIP simulation on 5 popular funds using actual NAV data from 2016-2026. The average investor in regular plans lost ₹1.58 lakh to commissions. Small cap funds were the worst — Nippon India Small Cap alone cost ₹2.43 lakh. Even "safe" large caps cost over ₹1 lakh.

The Question

Everyone says "direct plans are cheaper." But by how much, exactly? Not in percentages — in rupees. For the specific funds you probably own.

I wanted a concrete answer: if you'd been in direct instead of regular for the last 10 years, how much more money would you have today?

What I Did

I pulled actual daily NAV data from AMFI for 5 of India's most popular equity funds — one from each major segment. Then I simulated a ₹10,000/month SIP from January 2016 to May 2026 (125 installments, ₹12.5 lakh total invested) on both the direct and regular plan of each fund.

No assumptions. No projected returns. Just real NAVs, real dates, real math.

Funds analyzed: - HDFC Flexi Cap Fund (Flexi Cap) - SBI Large Cap Fund (Large Cap) - HDFC Mid Cap Fund (Mid Cap) - Nippon India Small Cap Fund (Small Cap) - ICICI Prudential Equity & Debt Fund (Hybrid)

The Findings

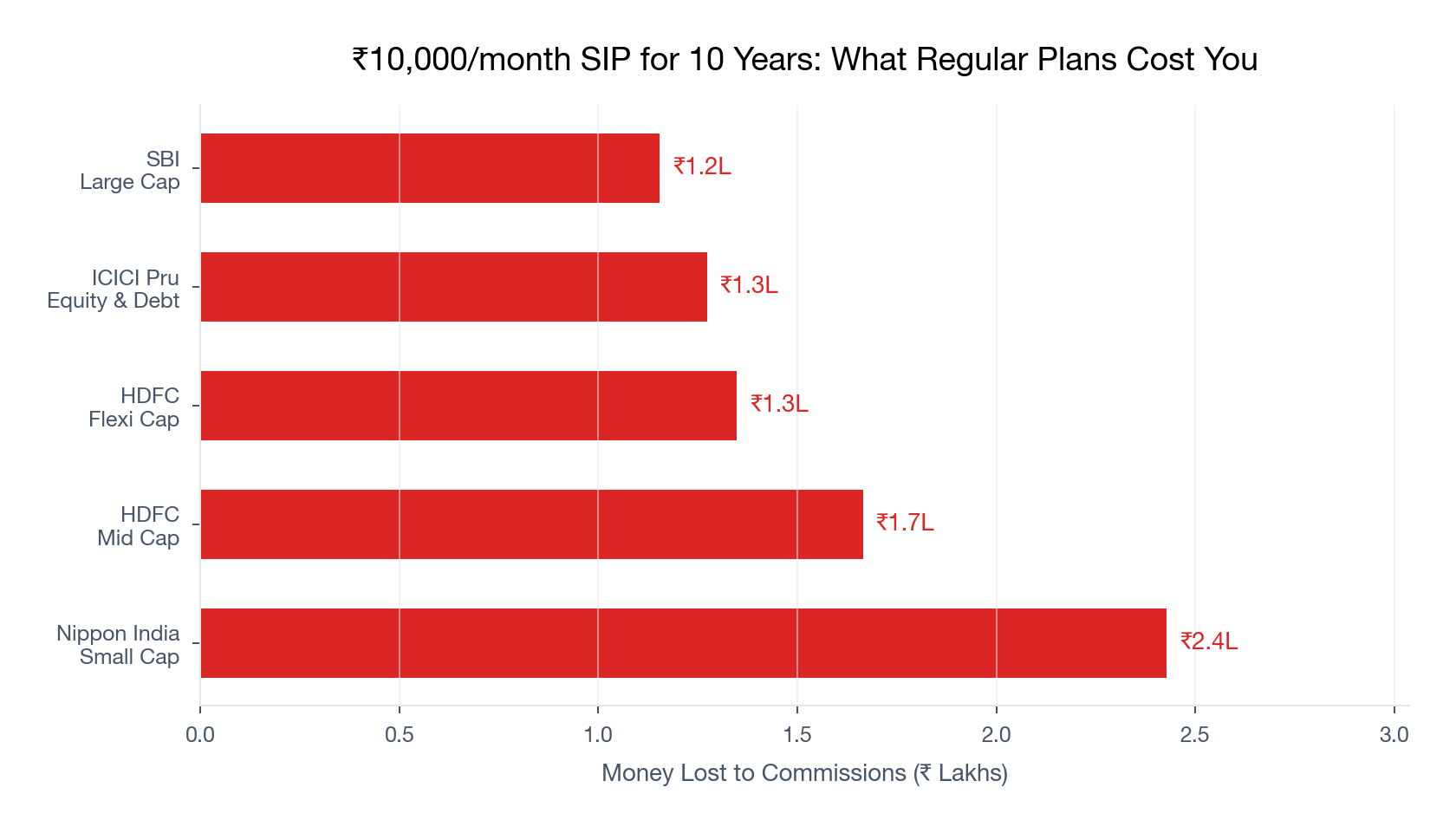

| Fund | Segment | Direct Corpus | Regular Corpus | You Lost |

|---|---|---|---|---|

| Nippon India Small Cap | Small Cap | ₹41.9L | ₹39.5L | ₹2.43L |

| HDFC Mid Cap | Mid Cap | ₹36.4L | ₹34.7L | ₹1.67L |

| HDFC Flexi Cap | Flexi Cap | ₹31.9L | ₹30.5L | ₹1.35L |

| ICICI Pru Equity & Debt | Hybrid | ₹31.0L | ₹29.7L | ₹1.28L |

| SBI Large Cap | Large Cap | ₹24.9L | ₹23.7L | ₹1.16L |

Average loss: ₹1.58 lakh across 5 funds. On ₹12.5 lakh invested, that's 12.6% of your entire investment gone to distributor commissions.

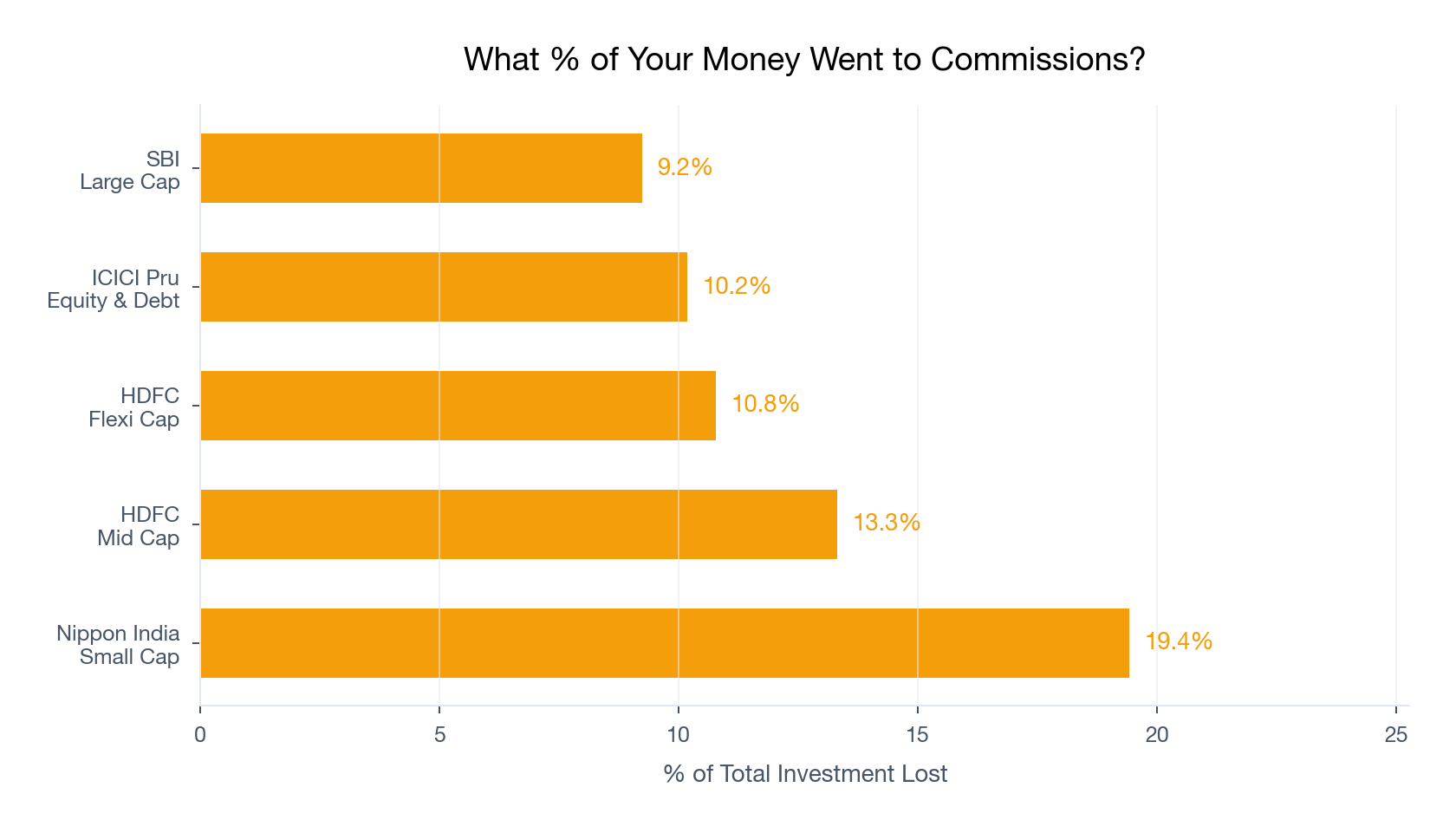

The Pattern: Smaller Caps = Bigger Damage

Small cap funds charge the highest expense ratios — and because they also deliver higher absolute returns, the compounding effect of that cost gap is amplified. Nippon India Small Cap's regular plan ate 19.4% of your total investment. Nearly one-fifth.

Large caps are the "least bad" at 9.2% — but that's still ₹1.16 lakh on a modest ₹10K SIP.

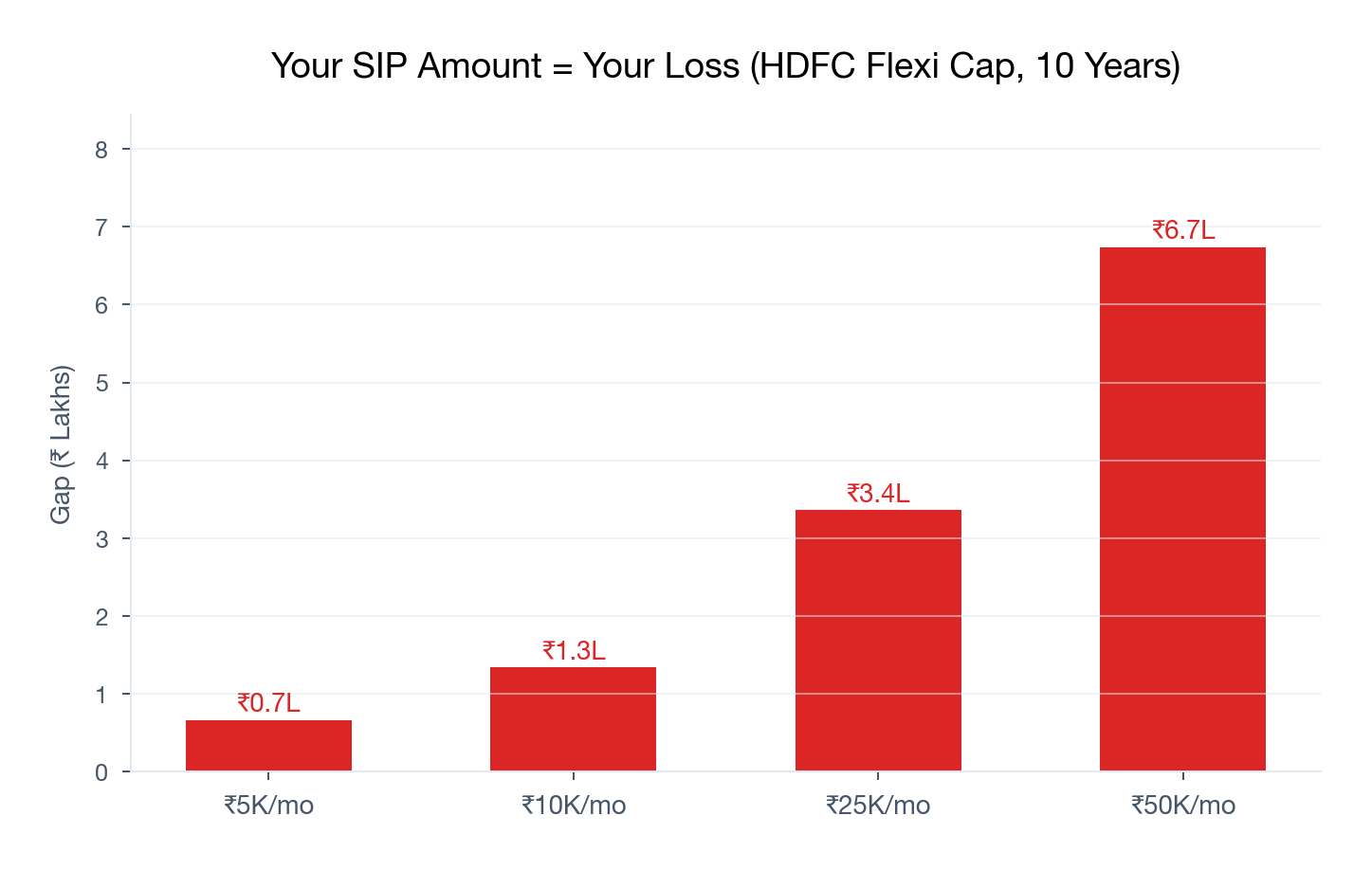

What If Your SIP Is Larger?

The gap scales linearly with your SIP amount:

| Your Monthly SIP | You Lost (HDFC Flexi Cap) |

|---|---|

| ₹5,000 | ₹67,500 |

| ₹10,000 | ₹1.35 lakh |

| ₹25,000 | ₹3.37 lakh |

| ₹50,000 | ₹6.75 lakh |

At ₹50K/month, you're losing ₹6.75 lakh in a single fund. If you hold 3-4 funds in regular plans, the total damage crosses ₹15-20 lakh easily.

What This Means For You

The "it's just 1%" narrative is a ₹1.5 lakh lie — at minimum. For small/mid cap investors or anyone with a larger SIP, it's much worse.

Three things to do:

-

Check which of your funds are in regular plans. Download your CAS from MFCentral — it shows the plan type for each holding.

-

Start all new SIPs in direct today. This costs nothing and has zero tax implications. Every month you delay is money lost.

-

Switch existing holdings gradually. If your gains are under ₹1.25 lakh, switch tax-free. Above that, switch in yearly tranches. Here's our step-by-step guide →

The Counterargument: When This Cost Is Worth Paying

Not everyone should switch. In our detailed comparison, we identified scenarios where regular plans genuinely make sense:

- You'd otherwise not invest at all. A distributor who moved you from FDs to equity earned that commission — 11% minus 1% still beats 6%.

- You panic-sell without guidance. Regular plan investors hold longer (21.2% held >5 years vs 7.7% in direct). If your distributor's phone call during a crash saved you from redeeming ₹30 lakh at the bottom, that's worth far more than ₹1.58 lakh.

- Your portfolio is under ₹5 lakh. The absolute gap is small, and a fee-only advisor would cost more.

The question isn't "is 1% too much?" — it's "am I getting ₹1.58 lakh worth of value over 10 years?" If your distributor does active goal planning, rebalancing, and crash-time handholding — maybe. If the relationship is an annual statement and a Diwali greeting — definitely not.

Try It With Your Own Numbers

We're building this exact analysis into Arth — plug in your funds, your SIP amounts, and see your personal ₹ gap in real-time. Try Arth →

Data: Actual daily NAV from AMFI via mfapi.in (Jan 2016 – May 2026) Method: Monthly SIP on 1st of each month (or next trading day), 125 installments Code: Available in our GitHub for verification

Run these numbers on your finances

Arth looks at your full picture and tells you what actually matters.

Try Arth →