In the new tax regime, NPS self-contributions get zero tax deduction. Only your employer's NPS contribution under Section 80CCD(2) remains deductible -- up to 14% of basic salary. If you're investing in NPS expecting a 2 lakh tax benefit and you're on the new regime, you're locking money until 60 for nothing.

That's the single most important fact about NPS tax benefits in 2026, and most guides bury it under pages of generic 80C explanation. This article gives you the exact sections, limits, and calculations for both regimes -- so you know precisely what NPS saves you (or doesn't).

Key Takeaways

- Old regime: up to 2L total deduction possible (80CCD(1) + 80CCD(1B) + 80CCD(2))

- New regime: ONLY Section 80CCD(2) employer contribution deductible (up to 14% of basic)

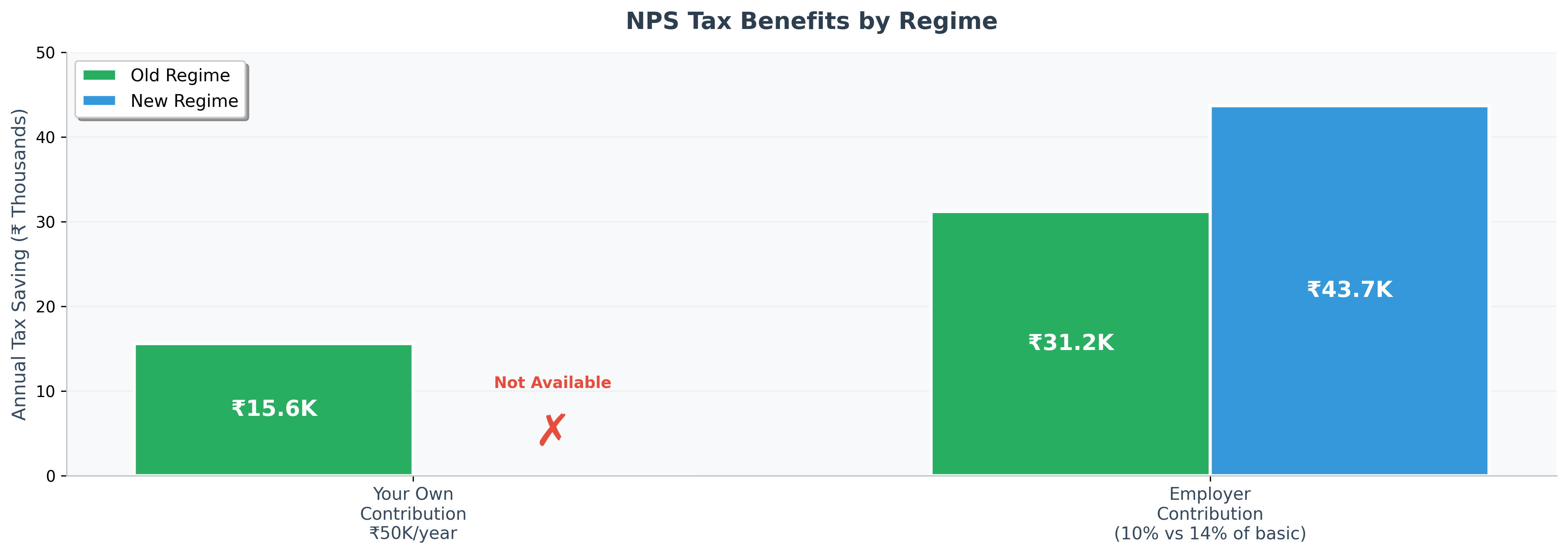

- The 80CCD(1B) extra 50,000 deduction saves 15,600/year at 30% bracket -- old regime only

- At withdrawal: 60-80% lump sum is tax-free, but annuity income is taxed at slab rate every year

- NPS is NOT fully EEE like PPF/EPF -- the annuity portion is taxed (making it EEE + EET hybrid)

NPS Tax Sections: The Complete Map

Before diving into regime-specific details, here's every tax section that touches NPS:

| Section | What it covers | Who claims it | Regime availability |

|---|---|---|---|

| 80CCD(1) | Employee self-contribution | You (salaried/self-employed) | Old only |

| 80CCD(1B) | Additional self-contribution | You | Old only |

| 80CCD(2) | Employer contribution | Your employer (you claim deduction) | Both regimes |

| 10(12A) | Employer contribution exemption | Automatic | Both regimes |

| 10(12B) | Partial withdrawal exemption | You (on withdrawal) | Both regimes |

| 10(12C) | Lump sum at maturity | You (on exit at 60) | Both regimes |

Now let's break each regime down with actual numbers.

Old Tax Regime: NPS Can Save You Up to 2 Lakh

Under the old regime, NPS offers three separate deduction buckets. Here's exactly how each works.

Section 80CCD(1): Your Self-Contribution (Within 80C Limit)

- What: Deduction for your own NPS Tier 1 contributions

- Limit: 10% of salary (Basic + DA) for salaried; 20% of gross income for self-employed

- Cap: Falls within the overall 1.5L limit of Section 80CCE (shared with 80C, 80CCC)

- Reality check: Most salaried employees already fill this 1.5L with EPF (mandatory) + PPF/ELSS/insurance. So 80CCD(1) typically adds zero incremental benefit.

Example: Ravi earns 12L/year (Basic + DA: 6L). His EPF contribution (1.44L) nearly fills the 80CCE limit. His NPS self-contribution under 80CCD(1) can only use the remaining 6,000 of the 1.5L cap. Practically useless.

Section 80CCD(1B): The Extra 50,000 (The Real NPS Incentive)

- What: Additional 50,000 deduction OVER the 1.5L 80CCE limit

- Limit: 50,000/year (hard cap)

- Key point: This is separate from and above the 80C/80CCE limit

- This is why people invest in NPS: It's the only way to get a deduction beyond 1.5L (other than health insurance under 80D)

Tax saved by bracket:

| Tax bracket | Tax saved on 50,000 (including 4% cess) |

|---|---|

| 5% (2.5-5L income) | 2,600 |

| 20% (5-10L income) | 10,400 |

| 30% (above 10L) | 15,600 |

At 30% bracket, 80CCD(1B) saves you 15,600/year. That's real money -- but you're locking 50,000/year until age 60 to get it. Over 30 years at 11% return (with a top NPS fund manager based on 5-year performance data), that 50K/year becomes ~96L in NPS. The 15,600/year savings reinvested at 10% becomes ~26L. Total benefit of the tax saving: approximately 26L over a lifetime. Is that trade-off worth it? It depends on your alternatives.

Section 80CCD(2): Employer Contribution (No Overall Cap)

- What: Deduction for your employer's NPS contribution

- Limit: Up to 10% of salary (Basic + DA) in old regime

- Key point: This does NOT fall under the 1.5L 80CCE cap -- it's a separate deduction

- Who pays: Your employer contributes from CTC, not from your take-home

Example: Neha's company offers to restructure her CTC to include ₹80,000/year NPS (10% of ₹8L basic). She chooses between:

Option A: Take ₹80K as salary → Pay ₹24,960 tax (39% bracket) → Invest ₹55,040 in MF

Option B: Put ₹80K in NPS → No upfront tax → Full ₹80K invested

The ₹80,000 under 80CCD(2): - Deducted from her taxable income (saves ₹24,960 vs taking as salary) - Doesn't touch her 1.5L 80C limit (EPF, PPF, ELSS still fully claimable) - Comes from CTC restructuring, not additional money

This is the best NPS tax benefit because the tax arbitrage (1.45x starting capital) beats mutual funds even with identical returns.

Total Deduction Possible (Old Regime)

| Component | Maximum amount |

|---|---|

| 80CCD(1) within 80CCE | Up to 1.5L (shared) |

| 80CCD(1B) additional | 50,000 |

| 80CCD(2) employer | 10% of salary (unlimited cap) |

| Practical maximum for most people | 50,000 (self) + employer contribution |

The theoretical "2L self-deduction" (1.5L + 50K) is misleading because 80CCD(1) shares space with EPF/PPF/ELSS. In practice, the incremental NPS benefit in old regime is: - 50,000 under 80CCD(1B) + employer contribution via CTC restructuring under 80CCD(2)

New Tax Regime: NPS Is Almost Pointless for Self-Contributions

Here's what changes when you're on the new regime (default since FY 2024-25):

What's NOT Available

| Section | Old regime | New regime |

|---|---|---|

| 80CCD(1) - self contribution | Yes | NO |

| 80CCD(1B) - extra 50K | Yes | NO |

| 80C (EPF, PPF, ELSS, LIC) | Yes | NO |

| 80D (health insurance) | Yes | NO |

| HRA exemption | Yes | NO |

What IS Available

| Section | Deduction | New regime limit |

|---|---|---|

| 80CCD(2) - employer contribution | Yes | Up to 14% of Basic + DA (enhanced from 10% in Budget 2024) |

| Standard deduction | Yes | 75,000 (enhanced from 50K in Budget 2024) |

The critical implication: If you're on the new regime and putting your own money into NPS, you get zero tax benefit. You're voluntarily locking money until 60, accepting lower returns than index funds, and getting nothing in return. Stop doing this.

Should You Switch Regimes Just for NPS?

Some people consider staying on the old regime specifically to claim the 80CCD(1B) deduction. Here's when that makes sense:

Switch to old regime for NPS ONLY if: - Your total old-regime deductions (80C + 80D + HRA + 80CCD(1B) + other) exceed the new regime's lower slab benefit - Typically requires total deductions above 3.75-4L/year - For income above 15L, old regime rarely wins even with NPS

Don't switch regimes just for NPS if: - Your only motivation is the 50K NPS deduction (saves 15,600, not enough to offset higher new-regime slabs) - You're under 10L income (new regime is almost always better) - You don't have HRA + significant 80C investments already

Not sure which regime is better for your salary structure? Arth calculates the optimal regime based on your actual deductions -- not generic rules of thumb.

Tax Treatment at NPS Withdrawal

At Age 60 (Normal Exit)

The tax treatment at exit is where NPS partially redeems itself:

| Component | Private sector | Government | Tax treatment |

|---|---|---|---|

| Lump sum | Up to 80% | Up to 60% | Fully tax-free |

| Annuity purchase | Minimum 20% | Minimum 40% | Tax-free at purchase |

| Annuity income | Monthly/yearly pension | Monthly/yearly pension | Taxed at slab rate |

The lump sum is genuinely tax-free under Section 10(12C). No conditions, no cap. If your NPS corpus is 1 crore at 60 (private sector), you can take 80L as lump sum with zero tax.

But the annuity income (from the 20% you're forced to buy) is taxed as salary income every year for life. This is the "T" in NPS's EEE+T hybrid tax treatment.

Before Age 60 (Premature Exit)

If you exit NPS before 60: - Only 20% as lump sum (tax-free) - 80% must buy annuity (if corpus > 5L) - Annuity income: taxed at slab rate

This makes early exit devastating. Your money is essentially trapped until 60 in any meaningful sense. Full withdrawal rules here.

Partial Withdrawal (Before 60)

- Amount: Up to 25% of your own contributions (not employer's)

- Tax: Fully tax-free under Section 10(12B)

- Conditions: After 3 years, specific reasons only, max 3 times ever

- No tax: Regardless of regime, partial withdrawals are exempt

NPS vs EPF vs PPF: Tax Comparison at Withdrawal

| Product | Contribution tax benefit | Growth | Withdrawal | Effective status |

|---|---|---|---|---|

| EPF | Yes (80C) | Exempt | Exempt (after 5 years) | EEE |

| PPF | Yes (80C) | Exempt | Fully exempt | EEE |

| NPS | Yes (old regime) | Exempt | Lump sum: exempt; Annuity: taxed | EEE + EET |

| ELSS | Yes (80C) | Exempt | LTCG 12.5% above 1.25L | EEE (mostly) |

NPS is the only retirement product where you're forced to take part of your withdrawal as taxable income for life. EPF and PPF are truly EEE with no strings attached.

NPS Vatsalya: Tax Benefits for Minor Children

Budget 2025 introduced NPS Vatsalya -- an NPS account for children below 18. Key tax points:

- Deduction: Parent can claim under 80CCD(1B) -- same 50,000 limit (old regime only)

- Lock-in: Until child turns 18, then converts to regular NPS Tier 1

- Contribution limit: Minimum 1,000/year

- At conversion: Child gets the corpus, regular NPS rules apply from 18 onwards

Arth's take: The tax benefit is identical to regular NPS (80CCD(1B), old regime only). But now you're locking a child's money until they're 60. Unless you specifically want a forced retirement corpus for your child that they can't touch for 42+ years, a PPF in the child's name (15-year lock-in, EEE) or equity mutual fund SIP (no lock-in, flexibility) is more practical.

Common NPS Tax Mistakes

Mistake 1: Claiming 80CCD(1B) in New Tax Regime

Your NPS contribution shows up in Form 16, and many people claim it while filing under new regime. The ITR processing system will reject this deduction or issue a defective return notice. If you're on new regime, do not claim 80CCD(1B).

Mistake 2: Double-Counting Within 80C

EPF contribution (employee share) already counts toward the 1.5L 80C limit. If your annual EPF is 1.44L (12% of 12L basic), you have only 6,000 remaining under 80CCE for NPS under 80CCD(1). Most people's NPS benefit comes only from 80CCD(1B) -- the extra 50K bucket.

Mistake 3: Forgetting Annuity Income Is Taxable

Many people plan their retirement income assuming NPS maturity is fully tax-free (like PPF). It's not. The annuity you receive monthly is taxed at your post-retirement slab rate. If your total income (including annuity + rental + interest) exceeds 3L in retirement, you'll pay tax on the annuity.

Mistake 4: Not Asking Employer for 80CCD(2) Restructuring

This is the biggest missed opportunity. Section 80CCD(2) works in BOTH regimes. If your employer offers salary restructuring to include NPS contribution (up to 14% of basic in new regime), you get: - Tax-free contribution (reduces taxable salary) - Same NPS growth - No personal money needed

Ask your HR specifically: "Can you restructure my CTC to include NPS employer contribution under 80CCD(2)?" Many IT companies, banks, and MNCs already offer this.

Mistake 5: Investing in NPS Tier 2 Expecting Tax Benefits

NPS Tier 2 has NO tax benefit for private sector employees. Only central/state government employees get Section 80C deduction on Tier 2 (with a 3-year lock-in). For everyone else, Tier 2 is just a mutual fund with lower returns and no tax advantage.

NPS Tax Benefit Calculator: Do Your Own Math

Here's the quick formula for each scenario:

Old regime, salaried (30% bracket): - 80CCD(1B) benefit: 50,000 x 0.312 = 15,600/year saved - 80CCD(2) benefit: [employer contribution] x 0.312 = [amount] saved - Total annual benefit: 15,600 + employer contribution saving

Old regime, salaried (20% bracket): - 80CCD(1B) benefit: 50,000 x 0.208 = 10,400/year saved

New regime (any bracket): - Self-contribution benefit: Zero - 80CCD(2) benefit: [employer contribution] x [your marginal rate] = [amount] saved

Self-employed (old regime, 30% bracket): - 80CCD(1): 20% of gross income (within 1.5L overall cap) - 80CCD(1B): additional 50,000 = 15,600 saved - No 80CCD(2) available (no employer)

Frequently Asked Questions

Can I claim both 80C and 80CCD(1B) together?

Yes. They are separate sections. 80C/80CCE has a 1.5L cap (EPF, PPF, ELSS, LIC, etc.). 80CCD(1B) gives an additional 50,000 above this cap. You can claim both -- total possible: 2L. But only in the old tax regime.

Is NPS Tier 2 tax-free?

For private sector employees, no. NPS Tier 2 has no tax benefit on contribution and gains are taxed at applicable rates on withdrawal (STCG/LTCG like debt funds). Only government employees get 80C benefit on Tier 2 contributions (with 3-year lock-in).

Is employer NPS contribution taxable for the employee?

No. The employer's contribution to your NPS under 80CCD(2) is exempt from your salary income (it doesn't get added to your taxable salary). It's also deductible as a separate deduction. Double benefit: not taxed as income AND gives a deduction.

How much tax can I save with NPS in the new regime?

On your own contributions: zero. The only NPS tax benefit in new regime is Section 80CCD(2)—employer contribution via CTC restructuring up to 14% of basic salary. If you take ₹80,000/year via NPS instead of as salary (39% bracket), you avoid ₹31,200 in upfront tax and invest the full ₹80K instead of ₹48.8K after tax.

Is NPS maturity amount fully tax-free?

Partially. The lump sum portion (60-80% depending on sector) is fully tax-free. But the annuity purchased with the remaining 20-40% generates monthly income that is taxed as salary at your slab rate. So NPS maturity is not fully tax-free like PPF or EPF.

Can I get NPS tax benefit if I'm self-employed?

Yes, in the old regime. Self-employed individuals can claim 80CCD(1) up to 20% of gross income (within 1.5L cap) and 80CCD(1B) for an additional 50,000. No 80CCD(2) is available since there's no employer. In the new regime, self-employed NPS contributions get zero deduction.

The Bottom Line on NPS Tax Benefits

The NPS tax story in 2026 is simple:

Old regime: NPS gives you an extra 50,000 deduction (80CCD(1B)) that no other product offers. At 30% bracket, that's 15,600/year -- a real benefit, though you're locking money for decades to get it.

New regime: NPS self-contributions give you nothing. Only employer contribution (80CCD(2)) has value. If you're investing your own money in NPS while on the new regime, you're getting zero benefit for a 30-year lock-in.

Either regime: Always take employer NPS contribution if offered. It's tax-efficient in both regimes and costs you nothing from take-home.

The tax benefit alone shouldn't drive your NPS decision. Read our complete guide to whether NPS is worth it -- we factor in returns, annuity drag, and alternatives to give you the full picture. Or upload your CAS to Arth and see how NPS fits into your complete retirement plan.

Sources: Income Tax India, ClearTax, PFRDA Last verified: June 2026 Note: Tax laws change periodically. Consult a tax professional for personalized advice.

Run these numbers on your finances

Arth looks at your full picture and tells you what actually matters.

Try Arth →