For most young professionals on the new tax regime, NPS is not worth it. Your self-contributions get zero tax deduction while your money stays locked until 60. The only unconditional yes: employer offers NPS via CTC restructuring—the tax arbitrage makes it unbeatable.

Most NPS guides lead with "save up to 2 lakh in tax!" without mentioning that only applies to the old tax regime—which most young professionals abandoned for the new regime's lower slab rates.

We're open source and earn zero commissions, so we can give you the regime-specific, math-backed verdict—including when the answer is "skip it."

Key Takeaways

- New regime: NPS self-contributions have ZERO tax benefit. Only employer contribution (80CCD(2)) is deductible.

- Returns reality: 63.6% of NPS funds beat Nifty 50 TRI vs 62.5% of large cap MFs over 5 years. Performance is virtually identical.

- Old regime + 30% bracket: Extra 50K deduction (80CCD(1B)) saves ₹15,600/year. Decent, not life-changing.

- Employer NPS: Always take it. It's CTC restructuring with tax arbitrage—₹1L/year becomes ₹1.43 Cr accessible vs ₹1.11 Cr if taken as salary.

- Forced annuity: 20% of corpus (private sector) must buy annuity at 5-5.5% rate. SWP from mutual fund gives 4x the income.

What NPS Actually Is

The National Pension Scheme is a government-backed retirement savings scheme with 2.22 crore subscribers and ₹16.6 lakh crore AUM (PFRDA, May 2026).

Your money goes into three asset classes: - Scheme E (equity): Invests in stocks, capped at 75% allocation - Scheme C (corporate bonds): Fixed-income corporate debt - Scheme G (government securities): Safest, lowest returns

Genuine advantages: - Ultra-low fees: 0.03-0.09% (vs 0.5-2.0% for mutual funds) - Tax arbitrage if you're in old regime or get employer contribution - Forced discipline (lock-in prevents impulsive withdrawals)

Genuine disadvantages: - Locked until 60 (unless you're on new MSF framework: 15 years) - Forced 20% annuity at exit (40% for government employees) - 75% equity cap (100% allowed under new MSF for new accounts only)

For detailed withdrawal rules, see our NPS withdrawal guide for private employees.

The Tax Regime Question: This Decides Everything

New Tax Regime: Almost Pointless for Self-Contributions

| Section | What it covers | Available in new regime? |

|---|---|---|

| 80CCD(1) | Your own contribution | ❌ NO |

| 80CCD(1B) | Extra ₹50K above 80C | ❌ NO |

| 80CCD(2) | Employer contribution | ✅ YES (up to 14% of basic) |

If you're on the new regime—which became default from FY 2024-25 and which most young professionals should be on—your self-contributions to NPS get zero tax deduction.

The only NPS tax benefit in new regime: employer contribution under 80CCD(2), enhanced to 14% of basic post-Budget 2024.

Old Tax Regime: Up to ₹2L Deduction Possible

| Section | Limit | Tax saved (30% bracket) |

|---|---|---|

| 80CCD(1) | Within ₹1.5L 80C cap | ₹0 (usually filled by EPF/PPF) |

| 80CCD(1B) | Extra ₹50K above 80C | ₹15,600/year |

| 80CCD(2) | Employer contribution (10% of basic) | Depends on contribution |

The real NPS incentive in old regime is 80CCD(1B): that extra ₹50,000 above the ₹1.5L limit. At 30% bracket, it saves ₹15,600/year.

For the complete tax breakdown with calculations, see our NPS tax benefits: old vs new regime guide.

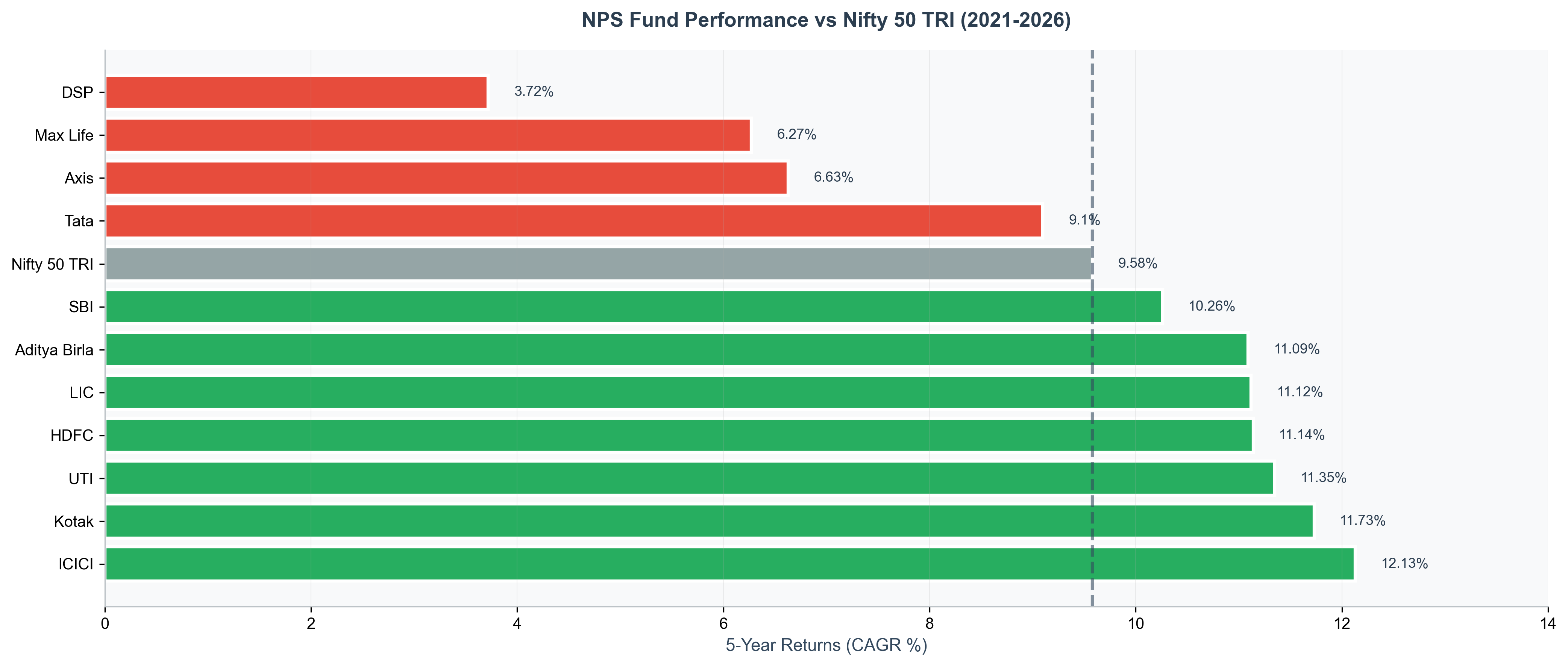

NPS Returns: The Data Nobody Shares

Every NPS article either bashes it ("underperforms!") or promotes it blindly ("lowest fees!"). We analyzed 5 years of verified NAV data to find the truth.

5-Year Performance (June 2021 - June 2026)

| Fund Manager | 5Y CAGR | vs Nifty 50 TRI (9.58%) | Result |

|---|---|---|---|

| ICICI Prudential | 12.13% | +2.55% | ✅ Beat |

| Kotak | 11.73% | +2.15% | ✅ Beat |

| UTI | 11.35% | +1.77% | ✅ Beat |

| HDFC | 11.14% | +1.56% | ✅ Beat |

| LIC | 11.12% | +1.54% | ✅ Beat |

| Aditya Birla | 11.09% | +1.51% | ✅ Beat |

| SBI | 10.26% | +0.68% | ✅ Beat |

| Tata | 9.10% | -0.48% | ❌ Lagged |

| Axis | 6.63% | -2.95% | ❌ Lagged |

| Max Life | 6.27% | -3.31% | ❌ Lagged |

| DSP | 3.72% | -5.86% | ❌ Lagged |

Result: 7 out of 11 funds (63.6%) beat Nifty 50 TRI.

7 out of 11 NPS funds beat Nifty 50 TRI over 5 years (2021-2026). Fund manager choice matters: 8.41% spread between best and worst.

7 out of 11 NPS funds beat Nifty 50 TRI over 5 years (2021-2026). Fund manager choice matters: 8.41% spread between best and worst.

How Does This Compare to Large Cap Mutual Funds?

We analyzed 24 large cap direct growth funds over the same period:

- Large cap MFs: 15 out of 24 (62.5%) beat Nifty 50 TRI

- Best MF performer: Nippon India at 15.70% (+6.12%)

- Worst MF performer: Axis at 7.45% (-2.13%)

Verdict: NPS and large cap MFs have virtually identical index-beating rates (1.1% difference). The "NPS underperforms" narrative is outdated.

For the complete 5-year analysis with methodology, see our NPS returns reality check.

Fund Manager Choice Matters

The spread between best (ICICI 12.13%) and worst (DSP 3.72%) is 8.41% annually. On ₹1L/year for 30 years: - With top performer: ₹2.83 Cr - With worst performer: ₹58 lakh - Difference: ₹2.25 Cr

You can change your NPS fund manager once per year for free. The switch takes 3-7 days and doesn't affect your accumulated corpus.

When NPS Makes Sense: The Decision Framework

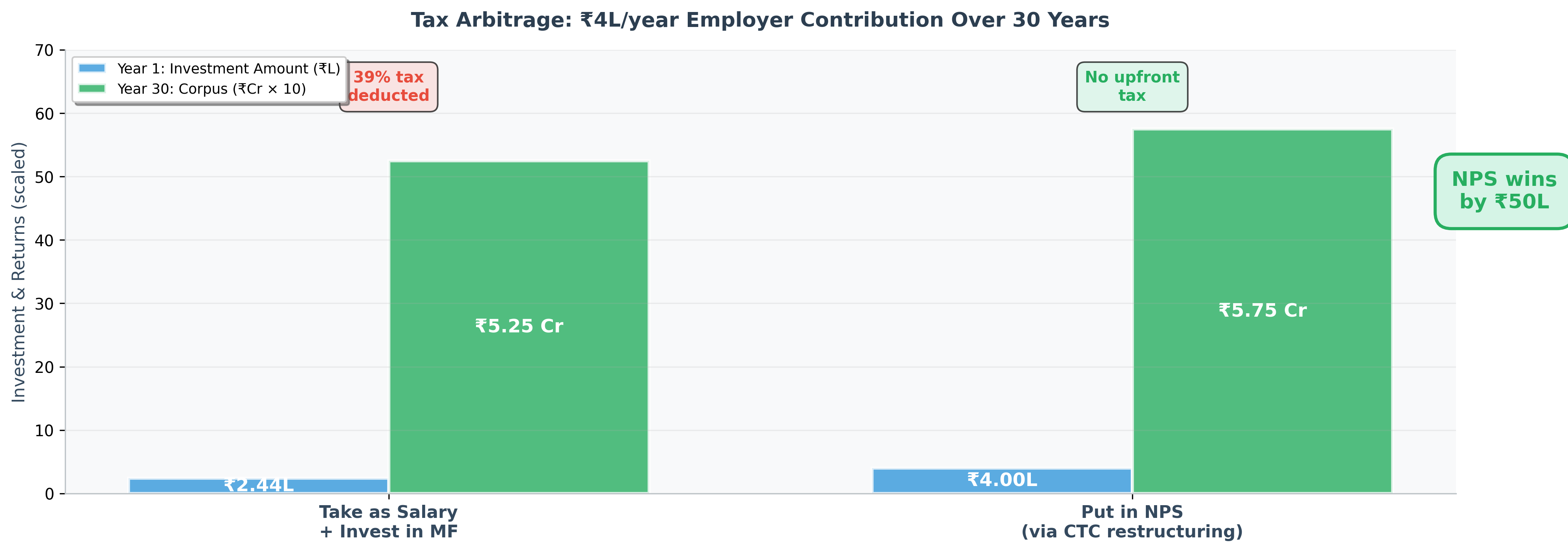

✅ Clear YES: Employer Offers NPS via CTC Restructuring

Rahul's company offers to restructure his CTC to include ₹1L/year NPS contribution (10% of ₹10L basic). This is part of his CTC—he has two choices:

Option A: Take as Salary + Invest in MF - Receive: ₹1L/year as salary - Tax (39% bracket): ₹39,000 - Net to invest in MF: ₹61,000

Option B: Put in NPS (80CCD(2)) - Goes to NPS: ₹1L/year (no upfront tax) - Full amount invested: ₹1L - Deductible from taxable income even in new regime

Starting capital ratio: ₹1L / ₹61K = 1.64x

Over 30 years at 11% (top NPS fund): - NPS corpus: ₹1L/year → ₹1.99 Cr - 60% tax-free: ₹1.19 Cr - 20% taxable at 39%: ₹40L - ₹15.6L tax = ₹24.4L net - 20% annuity: ₹40L → ₹2.2L/year pension (taxable) - Total accessible: ₹1.19 Cr + ₹24.4L = ₹1.43 Cr - MF corpus: ₹61K/year at 12% → ₹1.21 Cr → ₹1.11 Cr after LTCG tax - NPS wins by ₹32L due to tax arbitrage

Starting capital advantage: ₹1L in NPS vs ₹61K in MF after 39% tax. Over 30 years, this compounds to ₹32L more wealth despite identical returns.

The rule: If your employer offers NPS restructuring, always take it. The tax arbitrage advantage (1.64x starting capital) is massive. You're not getting "free money"—you're choosing the pre-tax route over the post-tax route.

⚠️ Conditional YES: Old Regime + 30% Bracket

Priya is 30, earns ₹15L/year (old regime, 30% bracket), has EPF + PPF filling her ₹1.5L 80C limit. She invests extra ₹50K/year in NPS for 80CCD(1B).

NPS Path (with tax benefit): - Annual investment: ₹50K - Tax saved: ₹15,600/year (30% + cess) - NPS corpus at 60 (11% CAGR, 30 years): ₹99.5L - 60% tax-free: ₹59.7L - 20% taxable at 30%: ₹19.9L - ₹6.2L tax = ₹13.7L net - 20% annuity: ₹19.9L - Tax savings reinvested at 10%: ₹26L - Total accessible: ₹59.7L + ₹13.7L + ₹26L = ₹99.4L

Index Fund Path (no tax benefit): - Annual investment: ₹50K - Corpus at 60 (12% CAGR, 30 years): ₹1.50 Cr - LTCG tax (12.5% on ₹1.35 Cr gains - ₹1.25L exempt): ₹16.7L - Net corpus: ₹1.33 Cr

Verdict: MF wins by ₹34L even in old regime. The ₹15,600/year tax saving (₹26L accumulated) doesn't overcome the return gap + better tax treatment.

For detailed scenarios, see NPS vs mutual fund for retirement.

❌ Clear NO: New Regime Self-Contributions

Same Priya, but on new regime. No 80CCD(1B) deduction. No ₹15,600/year tax saving. No ₹26L accumulated.

NPS in new regime: ₹73.4L accessible (₹59.7L tax-free + ₹13.7L taxable) - locked until 60, forced annuity Index fund: ₹1.33 Cr (fully liquid, no annuity)

Gap: ₹60L. You're giving up 45% more wealth AND locking your money for zero benefit.

There is no rational argument for voluntary NPS self-contributions in the new regime.

❌ Clear NO: FIRE Aspirants

If you might retire before 60, NPS premature exit is brutal: - 80% of corpus must go to annuity (vs 20% at normal exit) - Annuity at 5.5% on a ₹50L corpus = ₹2.75L/year - That's ₹23K/month—before tax—to live on in early retirement

Large cap MFs: withdraw anytime, zero penalty, full corpus available.

The Annuity Problem Nobody Talks About

At 60, private sector employees must put minimum 20% of corpus into an annuity (40% for government employees).

Current Annuity Rates

- Life annuity with return of purchase price: 5-5.5%/year

- Life annuity without return: 6-7%/year

Most people choose "with return" so their family gets the money back. That means 5.5% fixed annual payout.

The Math

Meera retires at 60 with ₹1 Cr NPS corpus. 20% annuity = ₹20L.

Annuity option: - ₹20L × 5.5% = ₹1.1L/year (₹9,167/month before tax) - At 30% tax: ₹6,417/month take-home - After 10 years at 6% inflation: worth ₹3,580 in today's money - Never increases

Mutual fund SWP option (4% on same ₹20L): - Year 1: ₹80K income - Year 10: ₹1.2L income (grows because remaining capital compounds) - Year 20: ₹1.8L income - Remaining capital at year 20: ₹25L (more than you started with)

SWP delivers 2-3x the lifetime income of the annuity, and you still have your capital.

Upload your portfolio to Arth and we'll show you exactly how your investments stack up against your retirement target.

The MSF Game-Changer (If You're Opening New Account)

In September 2025, PFRDA launched the Multiple Scheme Framework (MSF) for new NPS accounts:

MSF benefits: - 100% equity allocation allowed (no 75% cap) - Exit after 15 years (not age 60) - Same ultra-low fees (0.03-0.09%)

This fixes the two biggest structural problems. Under MSF, NPS should match or beat large cap MF performance while maintaining fee advantage.

The catch: MSF is only for new accounts opened under this framework. Existing legacy NPS accounts don't automatically get these benefits.

Frequently Asked Questions

Is NPS worth it in 2026 under the new tax regime?

For self-contributions, no. Under the new tax regime, you get zero deduction on your own NPS contributions. You're locking money until 60 with no tax advantage. Only employer contributions under 80CCD(2) remain beneficial.

Do NPS returns actually match mutual funds?

Yes. 5-year data shows 63.6% of NPS funds beat Nifty 50 TRI vs 62.5% of large cap MFs—virtually identical performance. The "NPS underperforms" narrative doesn't hold up against recent data. See our 5-year analysis for full details.

Should I take employer NPS contribution?

Always yes. It's CTC restructuring—you choose between taking it as salary (pay 39% tax, invest ₹61K in MF) or putting ₹1L in NPS (no upfront tax). The tax arbitrage advantage: over 30 years at 11%, NPS gives ₹1.43 Cr accessible vs MF's ₹1.11 Cr—₹32L more wealth.

Can I withdraw NPS before 60?

Partially, yes—but the rules are restrictive. You can withdraw 25% of your own contributions after 3 years, only for specified reasons (home purchase, education, medical, skill development), maximum 3 times in your lifetime. For complete exit before 60, 80% must go to annuity. Full withdrawal rules here.

What's the real downside of NPS?

Lock-in until 60 and forced 20% annuity at exit (private sector). Not returns—NPS delivers competitive equity returns. The trade-off is liquidity vs tax arbitrage, not performance.

What if I switch from old to new tax regime—do I lose NPS benefits?

You don't lose your NPS account or corpus. But you lose the tax deduction on self-contributions (80CCD(1) and 80CCD(1B)). Employer contributions under 80CCD(2) continue to be deductible. The withdrawal tax treatment remains the same regardless of regime.

The Honest Verdict

Is NPS worth it? The data tells a clear story:

NPS is worth it if: - Your employer offers NPS via CTC restructuring (unconditional yes—tax arbitrage gives you ₹32L more over 30 years on ₹1L/year) - You need forced discipline to not withdraw retirement savings (behavioral benefit has real value)

NPS is NOT worth it if: - You're on old regime making self-contributions (MF wins by ₹34L even with tax benefit)

NPS is not worth it if: - You're on new regime making self-contributions (zero tax benefit, full lock-in) - You're a FIRE aspirant who might retire before 60 (premature exit is brutal) - You value liquidity and hate forced annuities (MFs give you both)

The "NPS underperforms" myth is dead—64% of funds beat the index, matching large cap MFs. The decision comes down to tax situation and liquidity needs, not returns.

Want to see how NPS fits (or doesn't fit) into your specific retirement plan? Upload your portfolio to Arth—we'll analyze your MFs, EPF, PPF, NPS together, then show you exactly what you need to hit your retirement number.

Data Sources: PFRDA, NPS Trust, NPSNAV GitHub, mfapi.in, NSE Indices

5-year analysis period: June 2021 - June 2026

Nifty 50 TRI: 9.58% CAGR (official NSE data)

Last updated: June 4, 2026

Disclaimer: Past performance is not indicative of future results. This analysis is for informational purposes only, not investment advice.

Run these numbers on your finances

Arth looks at your full picture and tells you what actually matters.

Try Arth →