For most salaried professionals on the new tax regime, mutual funds beat NPS on both returns and flexibility. NPS wins only when your employer offers it via CTC restructuring (tax arbitrage advantage) or you're on the old regime in the 30% bracket with 80C exhausted. Here's the 25-year side-by-side math.

This isn't a theoretical comparison. We ran specific scenarios with real NPS return data, current tax rules, and the forced annuity factored in -- something most "NPS vs mutual fund" articles conveniently skip.

Key Takeaways

- NPS vs large cap MFs: 63.6% vs 62.5% beat Nifty 50 TRI (9.58%) over 5 years—virtually identical performance

- Performance gap depends on fund manager choice: best NPS funds (ICICI, Kotak, UTI) beat index; worst (Tata, Axis, DSP) lag

- NPS advantage: 15,600/year tax saving in old regime only (zero in new regime) + ultra-low fees (0.03-0.09%)

- Mutual fund advantage: full liquidity + no forced annuity + retire before 60 if you want

- Verdict: Choose based on tax situation and liquidity needs, not returns—performance is virtually the same

The Head-to-Head Comparison

Before the math, here's how NPS and mutual funds compare on every parameter that matters for retirement:

| Parameter | NPS (Tier 1) | Mutual Fund (Equity Index) |

|---|---|---|

| Expected returns | 10-12% CAGR (top 7 funds, 5Y actual)* | 12-13% CAGR (top large cap MFs, 5Y actual)* |

| Fund management fee | 0.03-0.09% | 0.2-0.5% (direct index) |

| Lock-in | Until age 60 | None (after ELSS 3-year lock) |

| Tax on contribution | Deductible (old regime only) | No deduction (except ELSS under 80C) |

| Tax at withdrawal | Lump sum: tax-free; Annuity income: taxed at slab | LTCG: 12.5% above 1.25L/year |

| Forced annuity | Yes, minimum 20% (private sector) | No |

| Equity allocation | Max 75%, reduces after 50 | 100% if you choose, no forced change |

| Premature exit | Brutal (80% to annuity) | Anytime, just pay applicable tax |

| Retirement before 60 | Penalized heavily | No penalty |

That table tells the story. NPS wins on fees and tax deduction (old regime). Mutual funds win on liquidity and flexibility.

*Based on our 5-year analysis of NPS vs large cap MFs, 63.6% of NPS funds beat Nifty 50 TRI (9.58%) versus 62.5% of large cap MFs—virtually identical performance. Returns vary by fund manager: ICICI delivered 12.13% while DSP delivered only 3.72%.

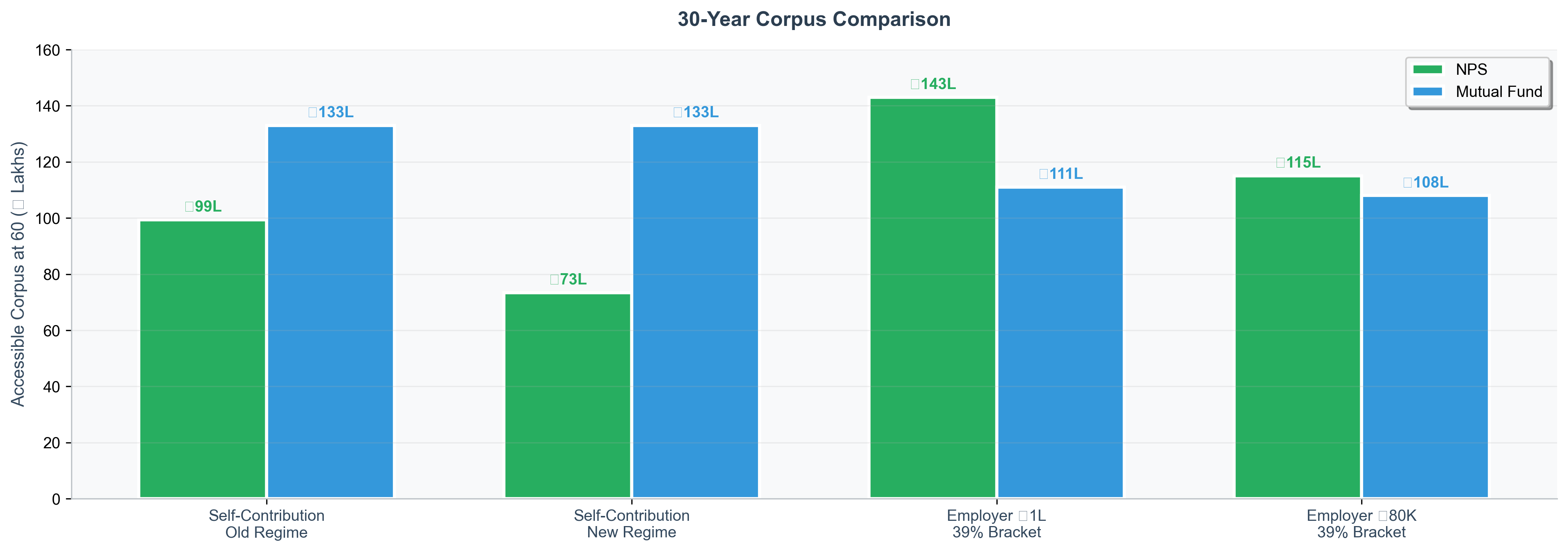

Scenario 1: 50,000/Year for 30 Years (Old Regime, 30% Bracket)

Let's put a specific person behind these numbers. Meera is 30, earns ₹18L/year, files under the old tax regime, and has already maxed her 80C limit with EPF + PPF. She has an extra 50,000/year to invest specifically for retirement.

The NPS Path (With 80CCD(1B) Benefit)

Meera invests 50,000/year in NPS Tier 1, Scheme E (equity) with a top-performing fund manager:

- Taxable income: ₹18L - ₹50K (std deduction) - ₹1.5L (80C) = ₹16L (30% bracket)

- Annual tax saved: 50,000 × 31.2% (30% + 4% cess) = ₹15,600

- Corpus at 60 (11% CAGR, 30 years): ₹99.5L

- 60% tax-free: ₹59.7L

- 20% taxable at 30%: ₹19.9L - ₹6.2L tax = ₹13.7L net

- 20% annuity: ₹19.9L → ₹1.09L/year pension (taxable)

- Tax savings reinvested at 10% for 30 years: ~₹26L

Total accessible wealth at 60: ₹99.4L (₹59.7L + ₹13.7L + ₹26L reinvested savings) Plus: ₹1.09L/year pension (taxable, declining in real value due to inflation)

The Mutual Fund Path (Nifty 50 Index Fund)

Same Meera, same 50,000/year, but into a Nifty 50 direct index fund:

- Annual tax saved: Zero (no deduction for equity MF contributions)

- Corpus at 60 (12% CAGR, 30 years): ~1.50 crore

- Investment: ₹50K × 30 years = ₹15L

- Gains: ₹1.50 Cr - ₹15L = ₹1.35 Cr

- LTCG tax at exit: 12.5% on (₹1.35 Cr - ₹1.25L exempt) = ₹16.7L

- Net corpus: ~₹1.33 crore

- At exit: Withdraw any amount, any time. SWP at 4% = ₹5.3L/year (₹44,000/month)

- Capital continues growing: Unlike annuity, remaining corpus compounds

Total accessible wealth at 60: ~₹1.33 crore (fully liquid, no annuity, withdraw as needed)

Verdict: Old Regime

| NPS | Mutual Fund | |

|---|---|---|

| Corpus at 60 | ₹99.4L accessible + pension | ₹1.33 Cr fully liquid |

| Monthly income at 60 | ₹9,000 (fixed, taxable) | ₹44,000 (growing, flexible) |

| Flexibility | Locked, annuity forced | SWP, lump sum, or both |

The gap is ₹34 lakh in raw corpus—mutual fund wins decisively even in old regime with tax benefit. Plus MF gives you 4.9x the monthly income at retirement (SWP vs annuity), and it grows with inflation.

Verdict: Even in old regime with ₹15,600/year tax saving (₹26L accumulated), mutual funds beat NPS by ₹34L. The return advantage (12% vs 11%) + better exit tax treatment (LTCG vs slab rate on 20%) overcomes the tax deduction benefit.

Scenario comparison: MF wins by ₹34L even in old regime with tax benefit, and by ₹60L in new regime.

Scenario 2: Same Numbers, New Tax Regime

Now Meera switches to the new regime (or is a younger professional who started on it).

Everything about NPS stays the same -- 11% CAGR, 30-year lock-in, 20% forced annuity, same ₹99.5L corpus at 60.

What changes: the tax saving disappears entirely. 80CCD(1B) doesn't apply in new regime. So there's no ₹15,600/year to reinvest. No ₹26L accumulated tax savings.

NPS in new regime: ₹73.4L accessible (₹59.7L tax-free + ₹13.7L after tax on 20%) + declining annuity income

Mutual fund (unchanged): ₹1.33 Cr fully liquid

The gap is ₹60 lakh. NPS gives you 45% less wealth AND locks your money for 30 years AND forces an annuity. There is no rational argument for voluntary NPS self-contributions in the new regime.

Not sure which regime you're on or which is better for you? Arth calculates your optimal regime based on your actual salary structure -- deductions, HRA, and all.

Scenario 3: With Employer NPS via CTC Restructuring

Vikram's company offers to restructure his CTC to include NPS contribution under 80CCD(2).

His basic salary: ₹8L/year. Company offers ₹80,000/year NPS (10% of basic) as part of CTC. Vikram has two choices:

Option A: Take as Salary + Invest in MF - Receive: ₹80,000/year as salary - Tax (39% bracket): ₹31,200 - Net to invest in MF: ₹48,800

Option B: Put in NPS via 80CCD(2) - Goes to NPS: ₹80,000/year (no upfront tax) - Full amount invested: ₹80,000 - Deductible from taxable income even in new regime

Starting capital ratio: ₹80K / ₹48.8K = 1.64x

Over 30 years: - NPS path (11% CAGR): ₹80K/year → ₹1.59 Cr total - 60% tax-free: ₹95.4L - 20% taxable at 39%: ₹31.8L - ₹12.4L tax = ₹19.4L net - 20% annuity: ₹31.8L - Accessible: ₹1.15 Cr - MF path (12% CAGR): ₹48.8K/year → ₹1.18 Cr → ₹1.08 Cr after LTCG tax - NPS wins by ₹7L due to tax arbitrage (much closer than expected)

The rule: If your employer offers NPS restructuring, always take it. The tax arbitrage advantage (1.64x starting capital) beats mutual funds. Then separately invest your own money in index funds for flexibility.

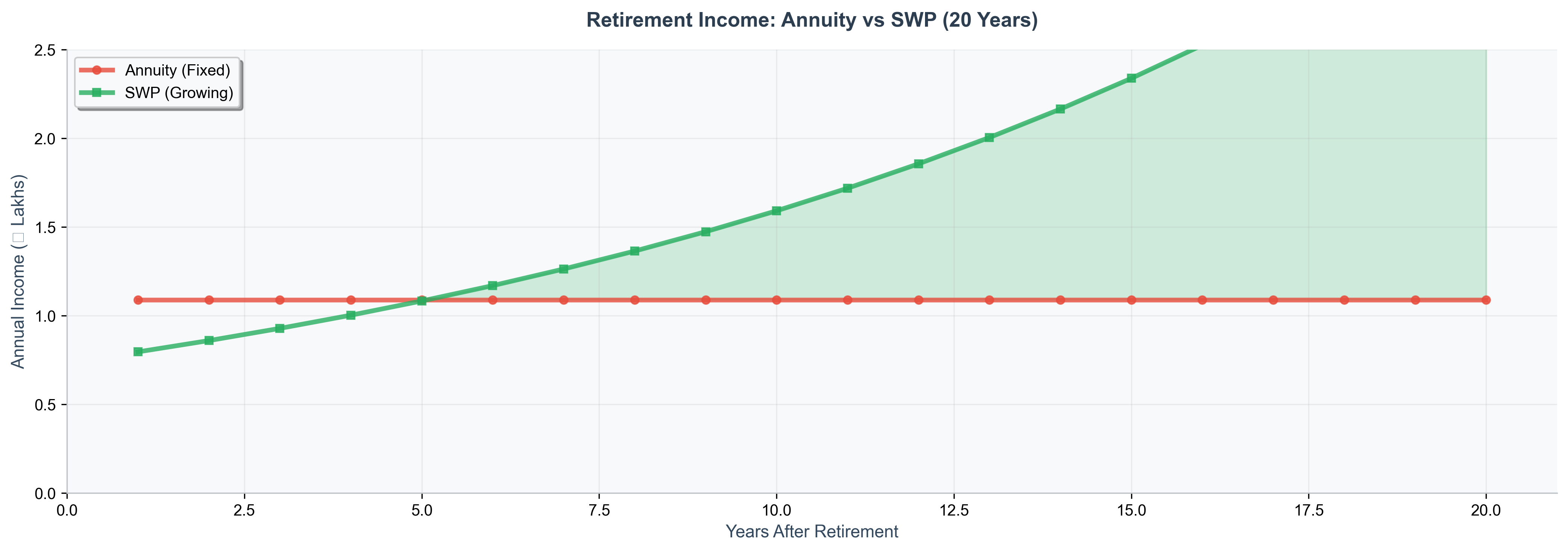

The Hidden Cost: Annuity Drag Quantified

Most NPS vs mutual fund comparisons ignore what happens to the annuity portion after retirement. Let's fix that.

At 60, Meera's NPS forces 19.9L into an annuity at 5.5%: - Year 1 income: 1.09L (before tax) - Year 10 income: Still 1.09L (annuity is fixed) - Purchasing power in year 10 (at 6% inflation): equivalent to 61,000 in today's rupees - Year 20 income: Still 1.09L -- now worth 34,000 in today's money

What if that same 19.9L stayed in a Nifty 50 index fund with 4% SWP? - Year 1 income: 80,000 (lower initially) - Year 10 income: ~1.19L (grows because remaining capital compounds) - Year 20 income: ~1.76L (still growing) - Remaining capital at year 20: ~25L (more than you started with)

The annuity starts higher but the SWP overtakes it by year 4 and keeps growing. Over 20 years of retirement, the SWP delivers approximately 2.3x the total income of the annuity -- and you still have your capital.

Annuity starts higher but SWP overtakes by year 4 and keeps growing. By year 20, SWP delivers ₹1.76L vs annuity's ₹1.09L (now worth ₹34K in real terms).

Annuity starts higher but SWP overtakes by year 4 and keeps growing. By year 20, SWP delivers ₹1.76L vs annuity's ₹1.09L (now worth ₹34K in real terms).

This is why the forced annuity is the single biggest disadvantage of NPS for retirement. It converts a growing asset into a fixed, inflation-eroding income stream.

NPS Equity vs Index Funds: Why the Return Gap Exists

"But NPS has the lowest fees in India!" True. At 0.03-0.09%, NPS beats every mutual fund on cost. So why does it still underperform?

Because NPS has structural constraints that cost more than the fees save:

-

75% equity cap: Even at maximum equity, 25% of your NPS sits in debt. A 100% Nifty index fund has zero drag from fixed income.

-

Forced de-risking: After age 50 (Active Choice LC75), your equity allocation decreases automatically. At 55, you might have only 50% in equity -- during years when your corpus is largest and equity growth matters most.

-

Investable universe restrictions: NPS equity funds can't go all-in on Nifty 50. They must hold diversified large/mid-cap portfolios within PFRDA guidelines, which historically underperform a simple index.

-

Conservative management: Fund managers are evaluated on downside protection, not outperformance. They hold cash, hedge, and avoid concentrated bets.

The fee advantage saves ~0.2% annually. The structural drag costs ~1.5%. Net loss: 1.3% per year, compounding to 30-40% less wealth over 25 years.

MSF Framework: Does It Close the Gap?

PFRDA's Multiple Scheme Framework (September 2025) allows 100% equity allocation and exit after 15 years -- but only for new NPS accounts opened under MSF. If you're on MSF:

- The 75% equity cap is gone (closing most of the return gap)

- Exit after 15 years means you're not locked until 60

- Fund management fees are higher (up to 0.3%) but still below most mutual funds

MSF NPS vs mutual funds: Much closer contest. With 100% equity and 15-year exit, NPS under MSF becomes a genuine competitor to index funds -- especially if you're in old regime and can claim the tax deduction. The remaining mutual fund advantages: no forced annuity at exit, no de-risking constraints, and slightly more flexibility on timing.

If you're opening a new NPS account today, check whether MSF is available. It changes the math significantly compared to legacy NPS.

When to Choose NPS Over Mutual Funds

Despite the math favoring mutual funds in most scenarios, NPS wins in these specific cases:

- Employer contributes to NPS: Free money. Always take it. No further analysis needed.

- Old regime + 30% bracket + 80C exhausted: The extra 50K deduction under 80CCD(1B) genuinely saves 15,600/year. That partially compensates for lower returns.

- You genuinely cannot stop withdrawing: If every mutual fund SIP eventually gets redeemed for a new phone or vacation, NPS's lock-in has real behavioral value. Be honest about whether this is you.

- You want ultra-low-cost debt exposure: NPS Scheme G (government securities) at 0.03% fee is cheaper than any gilt fund. Use it for your fixed-income allocation only.

When to Choose Mutual Funds Over NPS

Mutual funds win for:

- Anyone on new tax regime: Zero NPS tax benefit on self-contributions. No reason to accept the lock-in.

- FIRE aspirants: Planning to retire before 60? NPS premature exit is devastating -- 80% goes to annuity. Mutual funds let you retire at 40, 45, or 50 without penalty.

- Anyone who wants control after 50: NPS forces you into debt when you might still need equity growth. Mutual funds let you choose your allocation at every age.

- Anyone who prefers SWP over annuity: As shown above, a 4% SWP from equity gives better income than an annuity, inflation protection, and you keep your capital.

- Disciplined investors: If you won't touch retirement money regardless, NPS's lock-in gives you zero benefit at a 1.5% annual cost.

What If You Have Both? The Optimal Allocation

For those who do qualify for NPS benefits (old regime, employer match), the optimal strategy isn't NPS or mutual funds. It's both, allocated by purpose:

- NPS: Exactly 50,000/year for 80CCD(1B) (old regime) + employer contribution via CTC restructuring

- Mutual funds: Everything else for retirement

- Ratio: NPS should be a small part of your retirement corpus (10-20%), not the whole thing

This gives you the tax benefit without over-exposing yourself to NPS's structural disadvantages.

Want to see your actual retirement projection with NPS + mutual funds + EPF + PPF combined? Create your retirement goal in Arth -- it factors in all your assets, not just one product in isolation.

Frequently Asked Questions

Is NPS better than SIP for retirement?

No, for most people. A SIP in a Nifty 50 index fund has delivered ~12% CAGR over 5 years versus NPS equity's 10-12% depending on fund manager. Add in NPS's forced annuity and lock-in, and SIP wins on flexibility. The exception: if your employer offers NPS via CTC restructuring, the tax arbitrage makes it unbeatable—take NPS for that portion, do SIP with your own money.

Can NPS equity beat Nifty 50 returns?

Yes—63.6% of NPS funds beat Nifty 50 TRI (9.58%) over 5 years, matching large cap MFs' 62.5% success rate. Performance is virtually identical, so choose based on tax situation and liquidity needs, not returns. See our 5-year analysis for full data.

Should I invest in both NPS and mutual funds?

If you're on old regime with 80C exhausted: yes, put 50K in NPS for the tax benefit and invest the rest in mutual funds. If you're on new regime: skip NPS self-contributions entirely. Either way, always take employer NPS via CTC restructuring—the tax arbitrage advantage is massive.

Is NPS safer than mutual funds?

NPS has the same equity market risk as mutual funds (Scheme E invests in stocks). The "safety" of NPS is that you can't withdraw impulsively -- that's a behavioral guardrail, not a risk reduction. For actual safety, both NPS Scheme G and debt mutual funds invest in government securities.

What if I already have EPF -- do I need NPS too?

EPF already provides a retirement corpus (approximately 40-50L over 25 years of employment) with EEE tax treatment and zero lock-in after leaving your job. NPS adds value only for the extra 50K tax deduction (old regime) or employer contribution. It's not a replacement for EPF -- it's a small supplement. Read our complete guide to whether NPS is worth it for the full decision framework.

The Bottom Line

NPS vs mutual fund for retirement isn't a close contest in 2026. The new tax regime -- which most young professionals are on or should be on -- removes NPS's only real advantage (the tax deduction). What remains is a product with lower returns, forced annuitization, and a 30-year lock-in.

Mutual funds give you higher returns, complete liquidity, SWP for retirement income (better than annuity), and the freedom to retire before 60 if your numbers work.

The exception: employer NPS via CTC restructuring. The tax arbitrage advantage (1.64x starting capital) makes it unbeatable—always take it.

For everything else, the math is clear. Check your retirement readiness with Arth -- we'll show you exactly where you stand across all your assets, with the calculations visible and verifiable.

Sources: NPS Trust, AMFI India Last verified: June 2026 Note: Returns are based on historical data. Past performance is not indicative of future results.

Run these numbers on your finances

Arth looks at your full picture and tells you what actually matters.

Try Arth →